আপনি যখন কাউকে বলেন যে আপনি স্টক মার্কেটে একজন বিনিয়োগকারী তখন কি আপনাকে এই প্রশ্নটি জিজ্ঞাসা করা হয়েছে?

আমি জানি যে আমাকে এই প্রশ্নটি অসংখ্যবার জিজ্ঞাসা করা হয়েছে, যদিও নির্দিষ্ট শব্দগুলিকে ব্যাখ্যা করা হয়েছে।

যাইহোক, মূল বার্তা পরিষ্কার.

গড় খুচরা বিনিয়োগকারীরা কি তাদের নিজস্ব খেলায় পেশাদারদের পরাজিত করতে পারে?

ওয়ান আপ অন ওয়াল স্ট্রিটে , কিংবদন্তি বিনিয়োগকারী, পিটার লিঞ্চ, প্রকাশ করেছেন কীভাবে তার ‘অপেশাদার ফিডেলিটির মাল্টিবিলিয়ন-ডলার ম্যাগেলান ফান্ড পরিচালনার পদ্ধতি তাকে আমেরিকার এক নম্বর মানি ম্যানেজার এবং সর্বকালের সবচেয়ে সফল বিনিয়োগকারীদের একজন হয়ে উঠতে পরিচালিত করেছিল।

1977 সালের মে থেকে 1990 সালের মে পর্যন্ত লিঞ্চ ম্যাগেলানকে 29.06% বার্ষিক রিটার্নের নেতৃত্ব দিয়েছিলেন যা S&P 500 এর জন্য মাত্র 15.52% এর তুলনায়। বিষয়গুলিকে প্রাসঙ্গিক করতে, আসুন দেখি যে আপনি যদি ম্যাগেলানে $1 এবং $1 বিনিয়োগ করেন S&P 500।

তার মন্ত্র সহজ:

গড় বিনিয়োগকারীরা তাদের নিজস্ব ক্ষেত্রে বিশেষজ্ঞ হয়ে উঠতে পারে এবং অল্প গবেষণা করে ওয়াল স্ট্রিট পেশাদারদের মতো কার্যকরভাবে বিজয়ী স্টক বাছাই করতে পারে।

এই বিশাল প্রবন্ধে, আমি আশা করি পিটার লিঞ্চের বই থেকে আমি যে মূল টেকওয়েগুলি পেয়েছি, তা ভেঙে দেব, যথা – স্টক বিনিয়োগের জন্য পিটার লিঞ্চের সাধারণ নির্দেশিকা৷

পিটার লিঞ্চের শেখানো পাঠগুলিকে 5টি সহজ উপায়ে বিভক্ত করা যেতে পারে:

বইটির দ্বারা প্রচারিত প্রথম নিয়মটি হল একজনের জন্য পেশাদারদের কথা শোনা বন্ধ করুন৷ !

এর অর্থ হট টিপস, ব্রোকারেজ ফার্মের সুপারিশ এবং আপনার নিজের গবেষণার পক্ষে আপনার প্রিয় নিউজলেটার থেকে সর্বশেষ "মিস করা যাবে না" পরামর্শ উপেক্ষা করা।

প্রকৃতপক্ষে, অপেশাদার বিনিয়োগকারীর অনেকগুলি অন্তর্নির্মিত সুবিধা রয়েছে যেগুলিকে কাজে লাগানো হলে, তারা বিশেষজ্ঞদের এবং সাধারণভাবে বাজারকেও ছাড়িয়ে যাবে৷

এটি নিম্নলিখিত কারণগুলির কারণে হয়:

বিপুল পরিমাণ পুঁজিতে তাদের প্রবেশাধিকারের কারণে পেশাদারদের পকেট খুব গভীর। তবে এটি তাদের একটি অসুবিধায় ফেলে কারণ তারা ছোট থেকে মাঝারি বাজারের ক্যাপ স্টকগুলিতে বিনিয়োগ করতে অক্ষম। এটি তহবিলের সামগ্রিক কর্মক্ষমতার উপর অর্থপূর্ণ প্রভাব ফেলবে না।

এই কারণেই ওয়ারেন বাফেট ছোট সিগারের স্টকগুলিতে বিনিয়োগ থেকে পরবর্তীতে পুরো কোম্পানিগুলিকে কেনার দিকে রূপান্তরিত হন৷

গড় খুচরা বিনিয়োগকারীদের জন্য উপলব্ধ সুযোগগুলি বড় বিনিয়োগকারীদের তুলনায় অনেক বেশি। পাসির রিস পুকুরে মাছ ধরার তুলনায় এটি একটি সমুদ্র থেকে মাছ তোলার মতো।

আমরা শুধু এটা পুঁজি প্রয়োজন.

একটি অজানা কোম্পানিতে একটি অস্বাভাবিকভাবে বড় লাভ করার সুযোগ এবং একটি প্রতিষ্ঠিত কোম্পানিতে শুধুমাত্র অল্প পরিমাণ হারানোর নিশ্চয়তার মধ্যে, পেশাদাররা পরবর্তীতে ঝাঁপিয়ে পড়বে।

সাফল্য একটি জিনিস, তবে আপনি যখন ব্যর্থ হন তখন খারাপ না দেখা আরও গুরুত্বপূর্ণ। এর কারণ হল ফান্ড ম্যানেজাররা কর্মচারী এবং তাদের কাজ সম্ভবত তাদের কর্মক্ষমতার উপর নির্ভর করবে।

ক্লায়েন্টরা বরং এই খবর শুনতে চায় যে তারা DBS বা Keppel-এ ছোট হেরেছে বনাম Goodland Group Ltd-এ বড় জয় পেয়েছে।

এদিকে, গড়পড়তা ব্যক্তিদের জন্য, আমরা কেন এত সুপরিচিত কাউন্টার কিনেছি তা নিয়ে আমাদের ড্রিল করার জন্য ভোরবেলা বা গভীর রাত পর্যন্ত কেউ আমাদের ফোন করে না।

সম্ভাব্য প্রতিক্রিয়ার মুখোমুখি হওয়ার জন্য 20-মিনিটের দীর্ঘ ব্যাখ্যা স্ক্রিপ্ট প্রস্তুত না করেই আমরা আমাদের নিজস্ব সিদ্ধান্ত গ্রহণ করি।

পিটার লিঞ্চ এইভাবে বাজারে পারফর্ম করার জন্য এই ধরনের সুবিধাগুলিকে পুঁজি করতে আমাদের উত্সাহিত করেন কারণ আমরা আমাদের সময়কে আরও উত্পাদনশীলভাবে ব্যবহার করতে পারি৷

সবচেয়ে খারাপ, দুর্ভাগ্যজনক ঘটনায় স্টক ট্যাঙ্ক, আপনার পূর্বের রায়ের সমালোচনা করার জন্য কেউ থাকবে না যা একজনের বিনিয়োগের সিদ্ধান্ত এবং কর্মকে প্রভাবিত করতে পারে।

ফান্ড ম্যানেজাররা অন্য লোকেদের অর্থ পরিচালনা করেন এই কারণে, এই তহবিল পরিচালকদের তাদের নিষ্পত্তিতে কতটা মূলধন রয়েছে তা ক্লায়েন্টরাই সিদ্ধান্ত নেয়।

এই লোকেরা সাধারণত বুদ্ধিমান বিনিয়োগকারী হয় না এবং ভালুকের বাজারের সময় তাদের অর্থ ফেরত নেওয়ার প্রবণতা রাখে এবং ষাঁড়ের সময় তাদের অর্থ ফেরত দেয়। এটি একজনের যা করা উচিত তার ঠিক বিপরীত। এটি তহবিল ব্যবস্থাপককে অনেক বেশি পুঁজি থাকার দ্বিধায় ফেলে দেয় যখন সবকিছু খুব দামি হয় এবং খুব কম হয় যখন সবকিছু সস্তায় বিক্রি হয়।

ইতিমধ্যে, আমরা আমাদের নিজস্ব তহবিল ব্যবস্থাপক এবং কখন আমাদের পুঁজি পুট-ইন এবং পুল-আউট করব তা সিদ্ধান্ত নেওয়ার একমাত্র ক্ষমতা আমাদের রয়েছে। আমাদের মূলধনকে অর্থপূর্ণভাবে কৌশলগত করতে হলে এটি আমাদের একটি মূল সুবিধা দেয়।

আপনার পুঁজি বের করার জন্য কেউ আপনাকে ডাকবে না যখন আপনার দুর্বল হৃদয় ব্যতীত অন্য স্টক ট্যাঙ্ক যা আপনাকে উপেক্ষা করতে শিখতে হবে। (লিঞ্চ মনস্তাত্ত্বিক দিকটিকে একটি বিশাল গুরুত্ব দেয়, যা পরবর্তী বিভাগে কভার করা হবে)

বর্তমান সিস্টেমের অধীনে, একটি স্টক প্রকৃতপক্ষে আকর্ষণীয় নয় যতক্ষণ না অনেক বড় প্রতিষ্ঠান এর উপযুক্ততা স্বীকার করে এবং সমান সংখ্যক বিশ্লেষক (গবেষক যারা বিভিন্ন শিল্প এবং সংস্থাগুলিকে ট্র্যাক করে) এটিকে ক্রয় বা যুক্ত তালিকায় রাখে।

এর মানে হল যে স্টকের বিশ্লেষণ রিপোর্ট প্রকাশিত হওয়ার সময়, একজনকে নিশ্চিত হওয়া উচিত যে স্মার্ট মানি ইতিমধ্যেই তারা যে মূল্যের প্রতিবেদন করছে তার তুলনায় অনেক সস্তা এবং আকর্ষণীয় দামে স্টকটি কিনেছে।

অতএব, তাদের স্টকগুলি সনাক্ত করার জন্য প্রকাশিত এই জাতীয় "কিনুন" বা "যোগ করুন" প্রতিবেদনের উপর নির্ভর না করা ভাল এবং বরং নিজের মানদণ্ডের সাথে তাদের নিজস্ব স্টকগুলির জন্য স্ক্রিন করা উচিত।

আপনার নিজের বিনিয়োগের দিগন্তের তুলনায় এই ধরনের বিশ্লেষণ প্রতিবেদনের স্বল্প মেয়াদী দিগন্তের কারণেও এটি ঘটে। বিশ্লেষকরা তাদের স্টকগুলির রেটিংগুলি তাদের সেট করা মূল্য লক্ষ্যের উপর ভিত্তি করে এবং সাধারণত, এই লক্ষ্যগুলি 12-মাস (1 বছর) সময় ফ্রেমে সরবরাহ করা হয়।

বিনিয়োগকারীদের জন্য (সুইং-ট্রেডার নয়), এক বছরের জন্য স্টকের মালিকানা ঝুঁকিপূর্ণ।

আচরণগত অর্থনীতিবিদ ডি বন্ড এবং থ্যালার উপলব্ধি করেছিলেন যে লোকেরা যুক্তিযুক্তভাবে সিদ্ধান্ত নেয় না। তাদের সিদ্ধান্তগুলি বিকৃত করা হয়েছিল বিশাল পরিমাণে জ্ঞানীয় ত্রুটিগুলির সাথে তাদের লড়াই করতে হয়৷

এইভাবে, এক বছরের হোল্ডিং পিরিয়ড বিনিয়োগকারীকে বাজারের ওঠানামায় উন্মোচিত করে কারণ বাজারের শেষ পর্যন্ত প্রবাদের ওজনের যন্ত্র হিসাবে কাজ করতে সময় লাগে।

আমাদের ফ্যাক্টর-ভিত্তিক বিনিয়োগ গাইডে পিরিয়ড ধরে রাখার বিষয়ে আরও পড়ুন।

আমাদের সকলের বলার সুযোগ আছে, “এটি দুর্দান্ত; আমি স্টক নিয়ে ভাবছি” অনেক আগেই পেশাদার বিশ্লেষকরা এর আসল সূত্র পেয়েছিলেন।

আমাদের সকলের কিছু নির্দিষ্ট শিল্প, পণ্য এবং পরিষেবা রয়েছে যা আমরা গড় ব্যক্তির চেয়ে বেশি জানি। সম্ভবত আপনি গেমিং শিল্প সম্পর্কে আরও জানেন কারণ আপনি একজন লেভেল 99 জাদুকর নিনজা এবং আপনার স্পর্শ করা প্রতিটি গেমে আধিপত্য। সম্ভবত আপনি ফ্যাশন শিল্পে কাজ করছেন এবং সর্বশেষ প্রবণতার সাথে সিঙ্ক করছেন।

লিঞ্চ বলেছে যে গড় ব্যক্তি বছরে দুই বা তিনবার সম্ভাব্য সম্ভাবনার মুখোমুখি হয় - কখনও কখনও আরও বেশি।

নীচের লাইন হল যে আমাদের সকলের কাছে আমাদের দৈনন্দিন জীবনের মাধ্যমে সর্বজনীনভাবে তালিকাভুক্ত কোম্পানিগুলির মূল্যবান এবং প্রাসঙ্গিক তথ্য রয়েছে। এটি এমন তথ্য যা পেশাদাররা এখনও জানেন না বা অর্জন করতে 100 ঘন্টা গবেষণা করেছেন।

পিটার লিঞ্চ বলেন, মানবিক আবেগ আমাদেরকে ভয়ানক স্টক মার্কেট বিনিয়োগকারী করে তোলে।

অজ্ঞ বিনিয়োগকারী ক্রমাগত তিনটি সংবেদনশীল অবস্থার মধ্যে থেকে যায়:

তিনি/তিনি চিন্তিত৷ বাজার কমে যাওয়ার পর বা অর্থনীতির ক্ষয়ক্ষতি দেখা দেয়, যা তাকে দর কষাকষিতে ভালো কোম্পানি কেনা থেকে বিরত রাখে

তারপর, পরবর্তী ষাঁড়ের দৌড় আসার সাথে সাথে, সে বেশি দামে পুনরায় প্রবেশ করে এবং আত্মতৃপ্ত হয় কারণ তাদের হোল্ডিং বেড়ে যাচ্ছে। বর্তমান মূল্যের তুলনায় মৌলিক বিষয়গুলি পরীক্ষা করার জন্য, এটি অত্যধিক মূল্যবান এবং স্ফীত কিনা তা নির্ধারণ করার জন্য তার/তার যথেষ্ট উদ্বিগ্ন হওয়া উচিত (কিন্তু তিনি তা করেন না)।

অবশেষে, যখন তার/তার স্টকগুলি কঠিন সময়ে পড়ে যায় এবং দামগুলি সে যা দিয়েছিল তার নীচে নেমে যায়, তখন তারা ক্যাপিচুলেট করে এবং একটি স্নিটে বিক্রি করে।

অনেক লোক নিজেদেরকে “দীর্ঘমেয়াদী বিনিয়োগকারী বলে অভিহিত করে ” কিন্তু শুধুমাত্র পরবর্তী বড় ড্রপ (বা সামান্য লাভ) পর্যন্ত, যে সময়ে তারা দ্রুত স্বল্পমেয়াদী বিনিয়োগকারী হয়ে ওঠে এবং বিপুল লোকসান বা মাঝে মাঝে সামান্য লাভের জন্য বিক্রি হয়ে যায়।

কৌশলটি আপনার অন্ত্রের অনুভূতিগুলিকে বিশ্বাস করতে শেখা নয়, বরং সেগুলি উপেক্ষা করার জন্য নিজেকে শৃঙ্খলাবদ্ধ করা। যতক্ষণ পর্যন্ত কোম্পানির মৌলিক গল্প পরিবর্তন না হয় ততক্ষণ আপনার স্টকের পাশে থাকুন।

লিঞ্চ প্রতিশ্রুতি দেয় যে আপনি যদি বাজারের উত্থান-পতন, এবং সুদের হারের অন্তহীন জল্পনাকে উপেক্ষা করেন, দীর্ঘমেয়াদে, আপনার পোর্টফোলিও আপনাকে পুরস্কৃত করবে যদি আপনি মৌলিকভাবে সঠিক নির্বাচন করেন।

এমনকি ওয়ারেন বাফেটের সর্বকালের সর্বশ্রেষ্ঠ দীর্ঘমেয়াদী বিনিয়োগগুলির মধ্যে একটি (ওয়াশিংটন পোস্ট) প্রথম কয়েক বছরের জন্য সম্পূর্ণ হারানোর মতো লাগছিল৷

বাফেটের কেনার পরে ওয়াশিংটন পোস্টের স্টক প্রায় 20% কমে গেছে এবং তিন বছর ধরে সেখানে ছিল! এটি প্রায় $2.2 মিলিয়ন ডলারের একটি কাগজ-ক্ষতি ছিল। যাইহোক, ওয়ারেন আর্থিক বিবৃতি পুনর্বিবেচনা করেছেন এবং খুঁজে পেয়েছেন যে ব্যবসার মৌলিক বিষয়ে কোন উল্লেখযোগ্য পরিবর্তন হয়নি। এইভাবে তিনি পোস্টের প্রকৃত মূল্য উপলব্ধি করার জন্য বাজার ধরে রাখার এবং অপেক্ষা করার সিদ্ধান্ত নেন। 2007 সালের শেষ নাগাদ, পোস্টে তার শেয়ারের পরিমাণ বেড়ে US$1.4 বিলিয়ন হয়েছে যা 10,000% এর বেশি লাভ।

দুর্দান্ত দীর্ঘমেয়াদী রিটার্ন সহ স্টকগুলি স্বল্প মেয়াদে বিনিয়োগের জন্য সত্যিই বেদনাদায়ক হতে পারে।

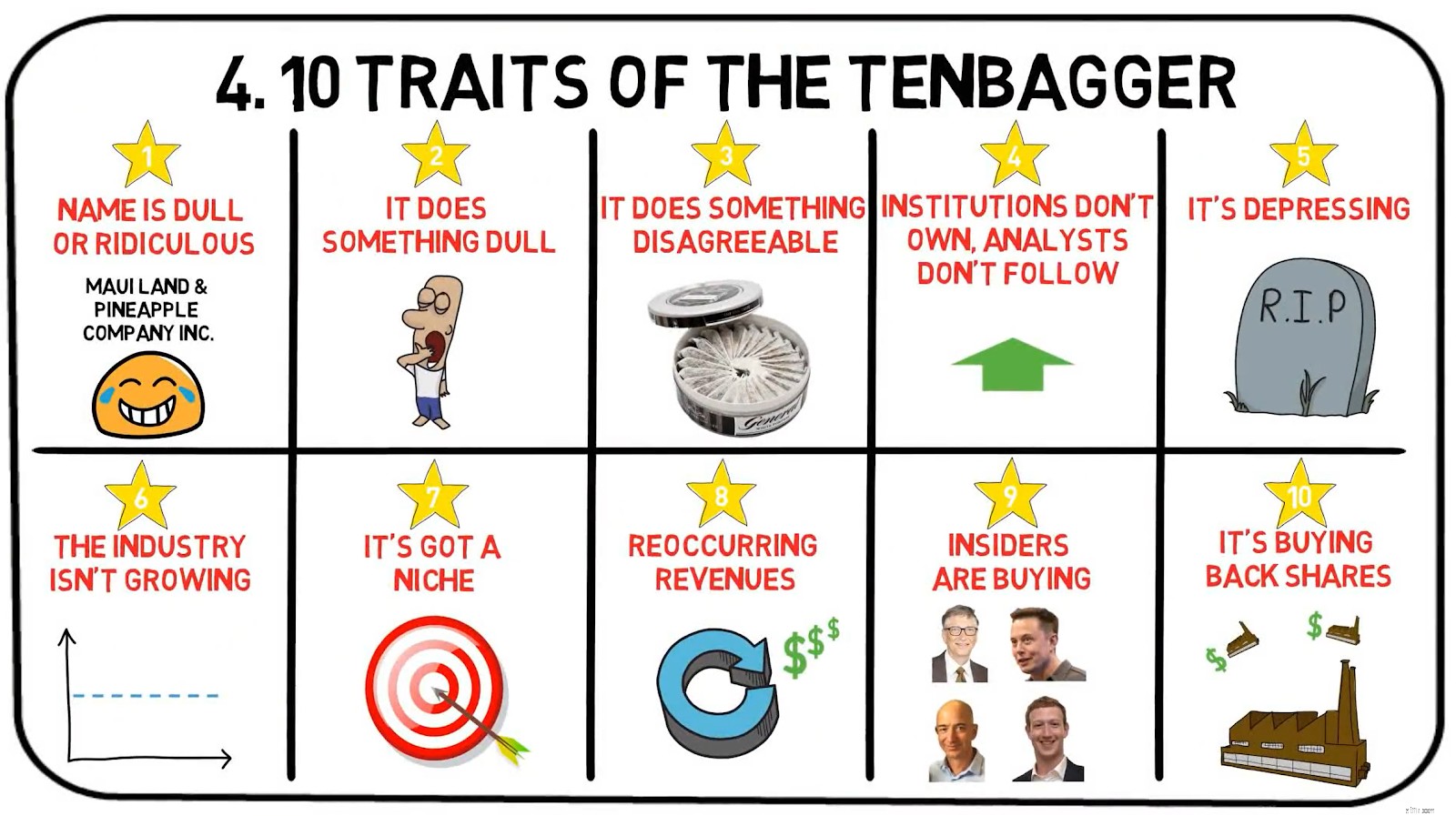

কিংবদন্তি 'টেনব্যাগার' হল লিঞ্চ একটি স্টক বর্ণনা করতে যে অভিব্যক্তিটি ব্যবহার করে যা আপনার ক্রয় মূল্যের দশগুণ প্রশংসা করেছে। ওয়ান আপ অন ওয়াল স্ট্রিটে, তিনি বেশ কয়েকটি বৈশিষ্ট্যের তালিকা করেছেন যা এই ধরনের টেনব্যাগারদের অন্তর্ভুক্ত করা উচিত।

তার বইতে, পিটার লিঞ্চ সকলের সর্বশ্রেষ্ঠ কোম্পানি নিয়ে এসেছেন - একটি আদর্শ লিঞ্চ টেনব্যাগার।

এই পৌরাণিক কোম্পানির নাম Cajun Cleansers.

এটি ছিল যাদুকরী সংস্থা পিটার লিঞ্চ একটি স্বপ্নের উদ্যোগের বৈশিষ্ট্য সম্পর্কে অধ্যায়ে বর্ণিত।

Cajun Cleansers আসবাবপত্র, বিরল বই এবং ড্র্যাপরিগুলি থেকে মৃদু দাগ অপসারণের বিরক্তিকর ব্যবসায় নিযুক্ত রয়েছে যা উপক্রান্তীয় আর্দ্রতার শিকার। নিউইয়র্ক বা বোস্টনের একজন বিশ্লেষক কখনোই ক্যাজুন ক্লিনজার পরিদর্শন করেননি বা কোনো প্রতিষ্ঠান তার শেয়ার কিনেনি।

একটি ককটেল পার্টিতে Cajun Cleansers উল্লেখ করুন এবং শীঘ্রই আপনি নিজের সাথে কথা বলবেন। এটা কানের মধ্যে সবার কাছে হাস্যকর শোনাচ্ছে।

দেশে দ্রুত প্রসারিত হওয়ার সময়, Cajun Cleansers-এর অবিশ্বাস্য বিক্রি হয়েছে। এই বিক্রয় শীঘ্রই ত্বরান্বিত হবে কারণ কোম্পানিটি একটি নতুন জেলের পেটেন্ট প্রকাশ করেছে যা জামাকাপড়, আসবাবপত্র, কার্পেট এবং বাথরুমের টাইলস থেকে সমস্ত ধরণের দাগ দূর করে। পেটেন্ট কাজুনকে সেই কুলুঙ্গি দেয় যা এটি খুঁজছিল।

কোম্পানি বার্ষিক কিস্তির সাথে আজীবন প্রেস্টেন বীমা অফার করার পরিকল্পনা করছে, যারা ভবিষ্যতের যেকোন পৃষ্ঠায় ঘটে যাওয়া সমস্ত দাগ দূর্ঘটনার গ্যারান্টিযুক্ত অপসারণের জন্য অগ্রিম অর্থ প্রদান করতে পারে।

সাত বছর আগে একটি আইপিওতে স্টকটি $8 এ খোলা হয়েছিল এবং শীঘ্রই $10 এ বেড়েছে। সেই মূল্যে গুরুত্বপূর্ণ কর্পোরেট পরিচালকরা তাদের সামর্থ্য অনুযায়ী শেয়ার কিনেছেন।

আমি কোম্পানী পরিদর্শন করি এবং জানতে পারি যে কোন প্রশিক্ষিত ক্রাস্টেসিয়ান জেল তৈরির তত্ত্বাবধান করতে পারে।

যদিও Cajun Cleansers একটি কাল্পনিক ব্যবসা, আপনি কিংবদন্তি ম্যাগেলান ফান্ড ম্যানেজারের চোখে টেনব্যাগার দেখতে কেমন তা অনুধাবন করতে পারেন। উপরে উল্লিখিত গল্পের বর্ণনাটি আমাদের মধ্যে বেশ কয়েকটি কোম্পানির ব্যবসায়িক মডেল এবং বিদ্যমান পরিবেশ থেকে খুব বেশি দূরে নয়।

হট স্টকগুলি দ্রুত বাড়তে পারে, সাধারণত মূল্যের যে কোনও পরিচিত ল্যান্ডমার্কের দৃষ্টির বাইরে, কিন্তু যেহেতু তাদের সমর্থন করার জন্য আশা এবং পাতলা বাতাস ছাড়া আর কিছুই নেই, তাই তারা ঠিক তত দ্রুত পড়ে যায়।

আসুন আমরা বেস্ট ওয়ার্ল্ডের দিকে তাকাই, একটি হট স্টক যা বনিতাস রিসার্চের একটি 28-পৃষ্ঠার প্রতিবেদন প্রকাশিত হওয়ার পরে যা প্রিমিয়াম স্কিনকেয়ার ফার্মের লাভের সত্যতা এবং বৈধতা নিয়ে প্রশ্ন তোলে৷

হটেস্ট ইন্ডাস্ট্রির সবচেয়ে সেক্সি স্টক ব্যতীত, এখানে স্টকের আরও 4টি বৈশিষ্ট্য রয়েছে যা পিটার লিঞ্চ অবশ্যই এড়িয়ে যাবেন:

কেউ যখন স্টকটিকে পরবর্তী "ফেসবুক" বা পরবর্তী "গুগল" হিসাবে আখ্যায়িত করে তখন সতর্ক থাকুন কারণ এটি প্রায় কখনওই হয় না।

প্রকৃতপক্ষে, এগুলি নিছক বিপণনের কৌশল এবং আপনাকে আরও পড়তে প্রলুব্ধ করার জন্য কৌশলীভাবে টোপ ক্লিক করুন।

"এই স্টক, কোম্পানি ABCXYZ, $2 শেয়ারে Facebook কেনার মত হতে পারে"

প্রায়শই না, তারা এই ধরনের স্টকগুলিকে বড় প্লেয়ারদের সাথে তুলনা করে এটিকে সম্পর্কযুক্ত করতে এবং অজ্ঞ বিনিয়োগকারীদের আকৃষ্ট করতে যারা শুনে শুনে ক্রয় করে।

এটি, ঘুরে, তাদের প্রলুব্ধ করে এবং পরবর্তী জিনিস যা আপনি জানেন, তিনি অবসর গ্রহণের জন্য তার সঞ্চয়ের অর্ধেক ABCXYZ-এর শেয়ার কেনার জন্য প্রতিশ্রুতিবদ্ধ করেন, তার বন্ধুদের কাছে ধোঁকা দিয়ে বলে যে তিনি তাড়াতাড়ি নৌকায় উঠেছিলেন।

কেউ কেউ এটিকে বৈচিত্র্য বলে, কিন্তু লিঞ্চ খারাপ সিদ্ধান্তকে Diআরও খারাপ হিসাবে আখ্যায়িত করতে পছন্দ করে ifying

শেয়ার ফেরত কেনা বা লভ্যাংশ বাড়ানোর পরিবর্তে, লাভজনক কোম্পানিগুলি প্রায়ই বোকা অধিগ্রহণে তাদের অর্থ উড়িয়ে দিতে পছন্দ করে।

প্রায়শই না, একজনকে অবশ্যই নিজেদেরকে জিজ্ঞাসা করতে হবে যে কোম্পানির সম্প্রসারণ মূল ক্রিয়াকলাপের সাথে সম্পর্কিত কিনা।

কিছু কাল্পনিক (অতিরিক্ত) উদাহরণ অন্তর্ভুক্ত করবে:

এখন, এটি মূর্খ মনে হবে, আপনি নিজের মনেই ভাবছেন যে কীভাবে এই ধরনের অধিগ্রহণের ধারণাটি পরিচালনা এবং নেতৃত্বের যাচাইয়ের মধ্য দিয়ে যেতে পরিচালিত হয়েছিল। কঠিন সত্য হল এই ধরনের জঘন্য বিস্তার বিদ্যমান।

আমরা যদি হাইফ্লাক্সের মানুষের বেদনাদায়ক পাঠটি আঁকতে পারি, আমরা স্পষ্টতই দ্বিমুখীকরণের একটি জটিল ঘটনা দেখতে পাব কারণ কোম্পানিটি জলের সমাধান উদ্ভাবন থেকে শক্তি এবং শক্তি উৎপন্ন করার জন্য প্রসারিত হয়েছে৷

সিঙ্গাপুর এবং এশিয়ায় প্রথম হওয়ায়, Tuaspring ইন্টিগ্রেটেড ওয়াটার অ্যান্ড পাওয়ার প্রজেক্টটি দক্ষতার মাত্রা বাড়াবে এবং ডিস্যালিনেশনের খরচ কমিয়ে দেবে বলে আশা করা হয়েছিল।

পাওয়ার প্ল্যান্টটি 2016 সালে খোলা হয়েছিল এবং এটি ছিল হাইফ্লাক্সের জ্বালানি ব্যবসায় প্রথম উদ্যোগ।

লক্ষ্য করুন কিভাবে Hyflux Tuaspring বাদ দিয়ে তাদের লাভ এবং উপার্জনের রিপোর্ট করতে বেছে নেয়?

এর কারণ হল Tuaspring কোম্পানির আয় এবং লাভের উপর একটি টানাপোড়েন, Hyflux বলেছে যে স্থানীয় জ্বালানি বাজারে "দীর্ঘদিন দুর্বলতা" এর ক্ষতির অন্যতম প্রধান কারণ।

এখানে সেই দুর্ভাগ্যজনক পাঠ সম্পর্কে আরও পড়ুন।

এই স্টকগুলিকে "লংশটস" বলা হয়।

তারা প্রায়ই অলৌকিক কিছু করার দ্বারপ্রান্তে বলে মনে করা হয় যেমন প্রতিটি ধরণের ক্যান্সার নিরাময় করা, গ্লোবাল ওয়ার্মিং সমাধান করা বা বিশ্ব শান্তি তৈরি করা।

হুইস্পার স্টকগুলির একটি সম্মোহনী প্রভাব রয়েছে এবং সাধারণত গল্পগুলির আবেগপূর্ণ আবেদন থাকে। এখানেই সিজল এতটাই উত্তেজনাপূর্ণ যে আপনি লক্ষ্য করতে ভুলে যাবেন যে কোনও স্টেক নেই।

অনেকটা এমএলএম স্কিমের মতো শোনায় যেখানে মোরিঙ্গা এলিক্সির যে কোনো ধরনের অসুস্থতার সমাধান করার প্রতিশ্রুতি দেয়...

এই সমস্ত লংশটগুলির মধ্যে যা মিল ছিল তা হল যে আপনি এগুলিতে অর্থ হারিয়েছেন তা হল এটির কোনও উপাদান ছাড়াই একটি দুর্দান্ত গল্প ছিল।

যে কোম্পানির বিক্রয়ের 25 - 50% একক গ্রাহকের উপর নির্ভরশীল তা একটি অনিশ্চিত পরিস্থিতিতে রয়েছে।

যদি একজন গ্রাহকের ক্ষতি একটি সরবরাহকারীর জন্য বিপর্যয়কর হয়, তার শীর্ষ লাইনে একটি বিশাল টোল থাকে, লিঞ্চ সরবরাহকারীতে বিনিয়োগ করতে সতর্ক থাকবে।

2018 সালে, AEM হোল্ডিংস তার একটি প্রধান গ্রাহকের উপর ব্যাপকভাবে নির্ভরশীল ছিল, যদিও কোম্পানির দ্বারা নির্দিষ্টভাবে চিহ্নিত করা হয়নি, বিশ্বাস করা হয় যে ইন্টেল, মার্কিন যুক্তরাষ্ট্রের অন্যতম বৃহত্তম চিপ নির্মাতা, যা প্রায় 93% অবদান রেখেছিল মোট রাজস্বের

এটিও একটি দুর্বল দর কষাকষির অবস্থান এবং কোম্পানিটি সম্ভবত এই একমাত্র গ্রাহক দ্বারা চাপা পড়ে যেতে পারে এবং এর প্রভাবের শিকার হতে পারে।

বইয়ের শেষ অধ্যায়ে, লিঞ্চ কিছু (সব নয়) গুরুত্বপূর্ণ বিষয়গুলির একটি সারাংশ চেকলিস্ট প্রকাশ করে যা তিনি স্টক সম্পর্কে আরও গভীরে যাওয়ার আগে জানতে চান।

পরিশ্রমী গবেষণা করার ক্ষেত্রে পিটার লিঞ্চের হোমস্পন সরলতার দ্বারা বিভ্রান্ত হবেন না - কঠোর গবেষণা ছিল তার সাফল্যের ভিত্তি।

একটি দুর্দান্ত ধারণার প্রাথমিক স্ফুলিঙ্গকে অনুসরণ করার সময়, লিঞ্চ বেশ কয়েকটি মৌলিক মান হাইলাইট করে যা তিনি আশা করেছিলেন যে কোনো স্টক কেনার জন্য পূরণ হবে।

যেমন একজন লক্ষ্য করবেন, পিটার লিঞ্চ কোয়ালিটেটিভ এ ডাইভ করার আগে গুণগত বিশ্লেষণ ব্যবহার করে একটি স্টক শনাক্ত করেন।

যাইহোক, ডঃ ওয়েলথ-এ, আমরা বিশ্বাস করি যে গুণগত দিকে থাকার আগে একটি স্টকের পরিমাণগত বিশ্লেষণ করা উচিত।

এইভাবে, আমরা যেকোনো মানসিক পক্ষপাতকে উপেক্ষা করতে পারি যা আপনার ক্ষতি করতে পারে।

আমরা হাইলাইট করতে চাই যে উভয় পন্থাই কাজ করবে, শুধু মনে রাখবেন আপনার গবেষণায় ভুলে যাবেন না।

সমস্ত স্টক গবেষণা একটি পরিমাণগত এবং একটি গুণগত উপাদান বহন করে।

আমরা আশা করি আপনি এখন পর্যন্ত দরকারী কিছু শিখেছেন। পরবর্তী কয়েক সেশনে, আমি পিটার লিঞ্চ ব্যবহার করা 3টি স্টক বিভাগে ডাইভিং করব। তারা হল:

মনে রাখবেন যে পিটার লিঞ্চের আসলে 6টি স্টক বিভাগ রয়েছে; ধীর চাষি, স্টলওয়ার্টস, দ্রুত উৎপাদনকারী, চক্রাকার, সম্পদের নাটক, পরিবর্তন।

এছাড়াও, আপনি যদি আমেরিকার এক নম্বর মানি ম্যানেজার দ্বারা আমার মতোই মুগ্ধ এবং প্রভাবিত হন, আপনি তার বই কেনার কথা বিবেচনা করতে পারেন। কিন্ডল সংস্করণগুলি সস্তা হতে পারে যদি ইলেকট্রনিকভাবে বই পড়া আপনার স্টাইল বেশি হয়।

যাই হোক, আমাদের কাঠামোবদ্ধ বিনিয়োগের কৌশল শেয়ার করার জন্য আমরা নিয়মিত প্রাথমিক কোর্স করি। আপনি যদি জানতে চান যে কীভাবে আমরা আমাদের নিজস্ব বৃদ্ধির স্টকগুলি খুঁজে পেতে আমাদের নিজস্ব কৌশলগুলির একটিকে একত্রিত করেছি, আপনি এখানে আরও শিখতে পারেন৷

Stalwarts হল প্রাক্তন দ্রুত বর্ধনশীল কোম্পানি যারা ধীর, আরও নির্ভরযোগ্য, বৃদ্ধির সাথে বড় কোম্পানিতে পরিণত হয়েছে (প্রতি বছর 3% প্রত্যাশিত গড় )

এছাড়াও, অটল কোম্পানিগুলি প্রয়োজনীয় এবং সর্বদা চাহিদাযুক্ত পণ্য উত্পাদন করে (ভাবুন খাদ্য, জল, বিদ্যুৎ, তেল ) , যা একটি মজবুত, স্থির নগদ প্রবাহ নিশ্চিত করে।

যদিও তারা বাজারের শীর্ষস্থানীয় পারফরমার হবে বলে আশা করা হয় না, যদি ভালো দামে কেনা হয়, স্টলওয়ার্টরা 4-5 বছরের হোল্ডিং পিরিয়ডে প্রায় 50% বা তার বেশি পরিমাণে উল্লেখযোগ্য লাভ অফার করে।

প্রয়োজনীয় পণ্য থেকে উত্পন্ন তাদের শক্তিশালী নগদ প্রবাহের কারণে, অচল ব্যক্তিরা সাধারণত একটি লভ্যাংশ দিতে সক্ষম হয়।

স্টলওয়ার্টের উদাহরণগুলির মধ্যে রয়েছে ম্যাকডোনাল্ডস, এসবিএস ট্রানজিট এবং প্রক্টর অ্যান্ড গ্যাম্বল।

উপরন্তু, পিটার লিঞ্চ স্টলওয়ার্টদের P/E বৃদ্ধির অনুপাত (PEG) 1.0-এর কম হওয়া প্রয়োজন। PEG অনুপাত একটি কোম্পানির মূল্য থেকে উপার্জন ভাগ করে গণনা করা হয় (PE) এর আয় বৃদ্ধির হার দ্বারা অনুপাত .

লিঞ্চ 1.0 এর নীচে PEG সহ কোম্পানিগুলিকে কম মূল্য হিসাবে বিবেচনা করে এবং 0.5 এর নীচে PEG সহ কোম্পানিগুলিকে একটি আসল দর কষাকষি বলে মনে করে৷ এটি বোঝা সহজ, যেহেতু আপনি যদি 1 এর কম পিইজি সহ একটি কোম্পানি কেনেন, তাহলে আপনি উপার্জন বৃদ্ধির এক ডলারের জন্য এক ডলারের কম প্রদান করছেন। এবং বেশির জন্য কম অর্থ প্রদান করাই হল সমস্ত বিনিয়োগের মূলনীতি।

লভ্যাংশ প্রদানকারী কোম্পানিগুলির জন্য, লিঞ্চ একটি ফলন-সামঞ্জস্যপূর্ণ PEG অনুপাতে পৌঁছানোর জন্য লভ্যাংশের ফলনকে আরও ফ্যাক্টর করে। ওয়ালমার্টকে প্রায়ই লিঞ্চের স্টলওয়ার্ট স্টক পদ্ধতির একটি ভালো উদাহরণ হিসেবে উল্লেখ করা হয়েছে।

এক সময়ে, Wal-Mart 20x PE এর কাছাকাছি লেনদেন করেছে। যার মানে গড় বিনিয়োগকারী $20 প্রতি ডলার উপার্জনের জন্য প্রদান করবে।

লিঞ্চ নির্ধারণ করেছে যে কোম্পানিটি এখনও 20-30% হারে বৃদ্ধি পাচ্ছে এবং বৃদ্ধির জন্য আরও অনেক জায়গা রয়েছে।

এর অর্থ হল একজন বিনিয়োগকারীর উপার্জনের আসল মূল্য আগামী কয়েক বছরের জন্য প্রতি বছর 20-30% কম হবে। $20 একটি দর কষাকষি ছিল. এবং ওয়াল-মার্ট হতাশ করেনি, পরবর্তী 20 বছর ধরে 20-30% বৃদ্ধি পাবে।

আমরা এখন Stalwarts এর কিছু বৈশিষ্ট্য জানি।

আমরা আমাদের স্টক নির্বাচনের সাথে অতিরিক্ত কঠোর হওয়ার জন্য কিছু অতিরিক্ত মানদণ্ড যোগ করেছি এবং আমাদের ফোকাসকে শুধুমাত্র সেরা স্টকগুলিতে সংকুচিত করেছি যা তদন্ত করা হবে। এই হল চূড়ান্ত মানদণ্ড যার জন্য আমরা সিঙ্গাপুরে Stalwarts খুঁজে পেতে ব্যবহার করব।

উপরের মানদণ্ডগুলি বরং স্ব-ব্যাখ্যামূলক হওয়া উচিত।

উপরের মানদণ্ডের পরিপ্রেক্ষিতে, আমরা 3টি স্টলওয়ার্টকে শর্টলিস্ট করেছি যেগুলিকে আমরা আজ কভার করব, যেগুলির উল্লেখযোগ্য বৃদ্ধির সম্ভাবনা রয়েছে বলে আমরা মনে করি৷ এছাড়াও, সমস্ত স্টকগুলিতে একজন টেনব্যাগারের নিম্নলিখিত এক বা একাধিক বৈশিষ্ট্য থাকবে, যা আপনার বিনিয়োগের 10X সম্ভাব্য রিটার্নের প্রতিনিধিত্ব করে।

| মার্কেট ক্যাপ। | $253M |

| ঐতিহাসিক লভ্যাংশ ফলন | 3% |

| সানসেট ইন্ডাস্ট্রিতে নয় | হ্যাঁ |

| PE অনুপাত | 21.73 |

| শিল্পের গড় পিই অনুপাত | 23.8 |

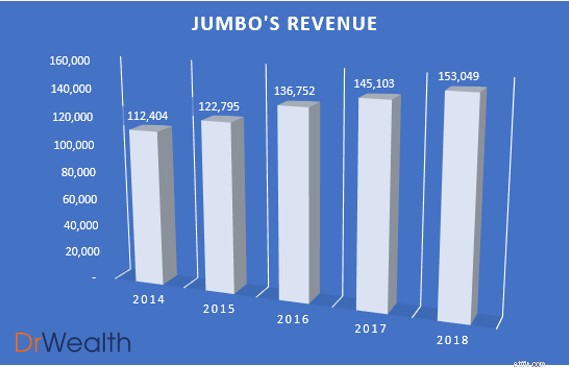

চার্টে দেখা গেছে, জাম্বোর আয় বছরে 5% বৃদ্ধির সাথে 2017 সালে $145m থেকে 2018 সালে $153M-তে বৃদ্ধি পেয়েছে৷

জাম্বো চীন এবং অন্যান্য অঞ্চলে আরও দৃঢ় অবস্থান অর্জনের দিকে নজর দেওয়ার কারণে আমরা সম্ভাব্যভাবে রাজস্ব বৃদ্ধির রক্ষণাবেক্ষণ বা এমনকি বাড়তেও আশা করব।

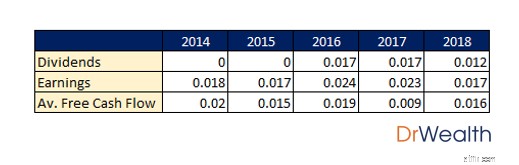

জাম্বো তার প্রাথমিক পাবলিক অফারিংয়ের পর থেকে বিগত 3 বছর ধরে লভ্যাংশ বিতরণ করছে এবং এর উপার্জন এবং বিনামূল্যে নগদ প্রবাহ 2017 ব্যতীত বিতরণ করা লভ্যাংশের চেয়ে বেশি।

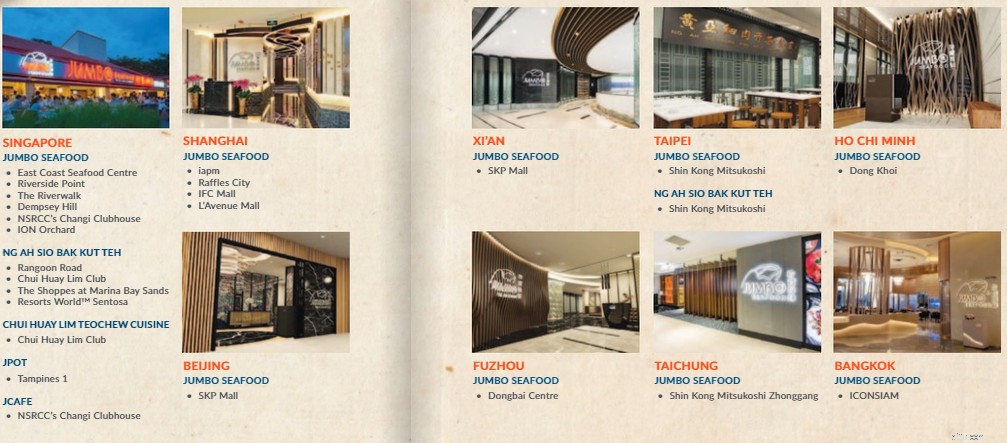

এটি বেইজিং, সাংহাই, তাইওয়ান এবং হো চি মিন সিটিতে এর অভূতপূর্ব বিস্তারের কারণে হয়েছিল। এটি 2017 সালে বিনামূল্যে নগদ প্রবাহের হ্রাস এবং 2018 সালে লভ্যাংশ বিতরণে পরবর্তী পতনকে সমর্থন করে৷

জাম্বো একটি ত্রি-মুখী পদ্ধতির সাথে এর বৃদ্ধির সম্ভাবনা মোকাবেলা করার লক্ষ্য রাখে:

এর রেস্তোরাঁর পোর্টফোলিওতে বৈচিত্র্য আনার মাধ্যমে, এটি তার সফল সীফুড ব্যবসায়িক মডেলের কিছু অংশকে অন্যান্য ব্র্যান্ড যেমন Ng Ah Sio Bak Kut Teh-এ প্রতিলিপি করতে সক্ষম। এইভাবে গ্রুপের জন্য আরেকটি লাভজনক উদ্যোগ হতে পারে যদি তারা এটিকে ভালোভাবে সম্পাদন করতে সক্ষম হয়। জাম্বো চীনে এনজি আহ সিও বাক কুট তেহকে পরিচয় করিয়ে দিতে চায় এবং আগামী 12 মাসের মধ্যে তাইওয়ানে কমপক্ষে আরও একটি এনজি আহ সিও বাক কুট তেহ আউটলেট এবং সিঙ্গাপুরে আরও একটি সুই ওয়াহ হংকং-স্টাইলযুক্ত "চা চান টেং" আউটলেট খুলবে। .

অধিকন্তু, বিদেশী ভোক্তা বাজারে বিস্তৃতির মাধ্যমে, জাম্বো একটি বৃহত্তর ঠিকানাযোগ্য ভোক্তা বেসের কাছে উন্মুক্ত হয়।

তারা যদি সিঙ্গাপুরের মতো সফলভাবে তাদের ব্র্যান্ড তৈরি করতে সক্ষম হয়, তাহলে গ্রুপের সামনে উজ্জ্বল সম্ভাবনা থাকবে।

দ্য এজ সিঙ্গাপুর আজই রিপোর্ট করেছে যে জাম্বো সিউলের গ্যাংনামে তার প্রথম ফ্র্যাঞ্চাইজড আউটলেট খুলেছে। এটি ব্যাংকক, ফুঝো, হো চি মিন, তাইপেই এবং তাইচুং-এ ফ্র্যাঞ্চাইজড আউটলেট সহ এশিয়া জুড়ে জাম্বো সীফুডের সংখ্যা 18 এ নিয়ে এসেছে।

জাম্বোর বিনিয়োগ এবং চীনে সম্প্রসারণ পাকা হতে শুরু করেছে কারণ এটি বর্তমানে প্রায় এর আয়ের 20.4% জন্য দায়ী। এই ধরনের পরিসংখ্যান চীনে এর সাফল্যের একটি শক্তিশালী প্রমাণ।

নেতৃত্ব এবং ব্যবস্থাপনা যদি চীনের মতো সফলভাবে তাদের আউটলেট সম্প্রসারণের মাধ্যমে বিভিন্ন অঞ্চলে তাদের বাজারের অবস্থান তৈরি করে, তাহলে আমরা সম্ভাব্যভাবে কোম্পানির বিক্রয়ের অভূতপূর্ব বৃদ্ধি দেখতে পাব।

হোম বেসে, যা এখনও কোম্পানির আয় বৃদ্ধির ভিত্তি তৈরি করে, জাম্বো ION Orchard-এ একটি আউটলেট খুলেছে।

এটি অর্চার্ডে তাদের প্রথম রেস্তোরাঁ হিসেবে একটি উল্লেখযোগ্য মাইলফলক চিহ্নিত করে, প্রিমিয়াম শপিং এবং বিনোদন বেল্ট৷ এটি দেখায় যে জাম্বো যখন বিদেশী সম্প্রসারণের মাঝখানে রয়েছে, তখনও এটি প্রাসঙ্গিক থাকার এবং স্থানীয় বাজারে বিস্তৃত হওয়ার জন্য এটির বিক্রয়ের মূল উত্স বজায় রাখার জন্য একটি বিন্দু তৈরি করে।

এটি একটি কুলুঙ্গি পেয়েছে

জাম্বো নামটা শুনলেই যে ছবিটি প্রথমে আপনার মনে ভেসে ওঠে সেটি অবশ্যই একটি মরিচ কাঁকড়া/মরিচ কাঁকড়া। এটি ঠিক জাম্বোর নিশ, সিঙ্গাপুরের একটি আইকনিক/ বিখ্যাত স্থানীয় খাবার বিক্রি করে এবং এর জন্য বিখ্যাত।

তাদের মরিচ কাঁকড়ার দক্ষতাকে সম্মানিত করা ছাড়াও, একটি নিশ থাকা জাম্বোকে খুব মুখের বন্ধুত্বপূর্ণ করে তোলে, যার অর্থ আপনার ব্যবসা সম্পর্কে কথা বলার আরও সুযোগ।

জাম্বোর মতো রেস্তোরাঁর জন্য এর সমকক্ষদের তুলনায় এই ধরনের প্রতিযোগিতামূলক সুবিধা থাকা গুরুত্বপূর্ণ যা একটি অত্যন্ত প্রতিযোগিতামূলক F&B শিল্পে থাকে। This ensures that its sales would not be affected immensely in the presence of new seafood entrances due to high customer retention rates.

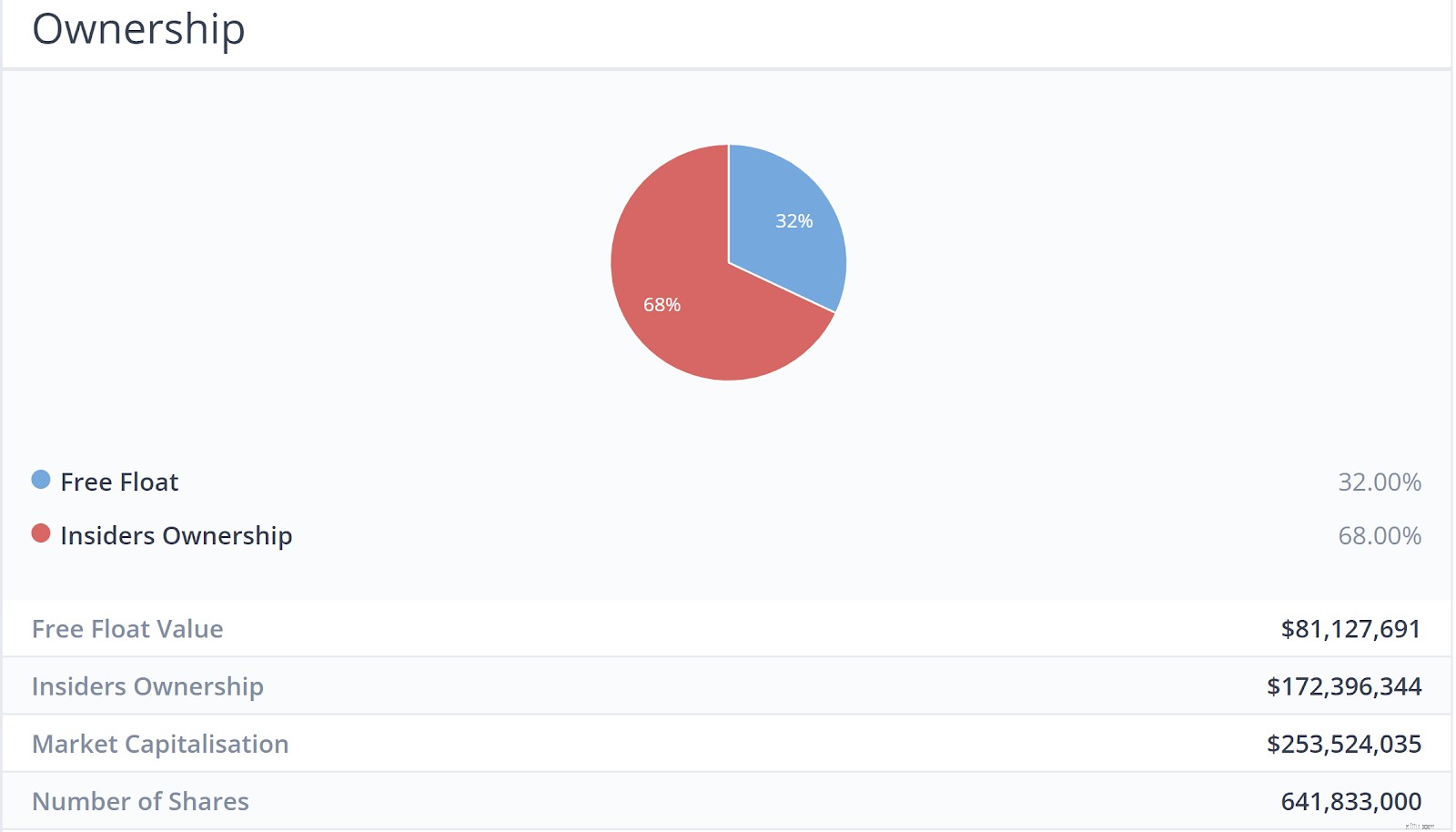

Skin in the Game (Insiders are buying/owning shares)

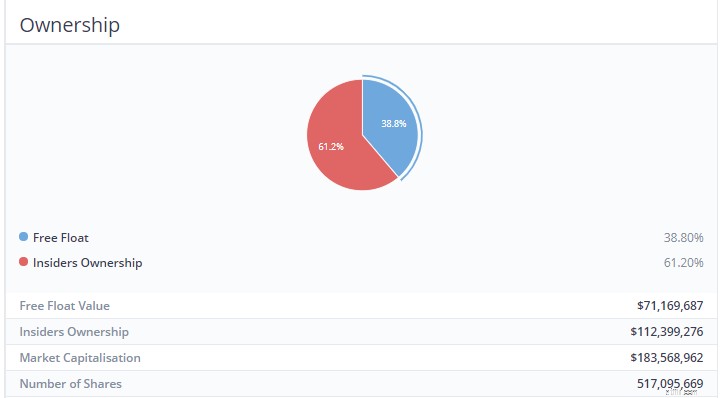

If the Chairman or the CEO of a company owns more than 50% of shares in the company, their interests are more likely to be more aligned with the shareholders.

That is because they are unlikely to take actions to harm their own wealth and would look towards improving the prospects of the company.

As can be seen, insiders of the company owned a majority of the shareholder-ship. Therefore, it proves that the management has skin in the game.

The Company is buying back Shares

Buying back shares is the simplest and best way a company can reward its investors, according to Peter Lynch.

If it has faith in its own future, then it would invest in itself, just as shareholders do.

Jumbo has been doing just that, posting notices from 31st May – 11th June on their daily share buy-backs.

| Market Cap. | $81M |

| Historical Dividend Yield | 4.27% |

| Not in Sunset Industry | Yes |

| PE Ratio | 24.22 |

| Industry Average PE ratio | 23.8 |

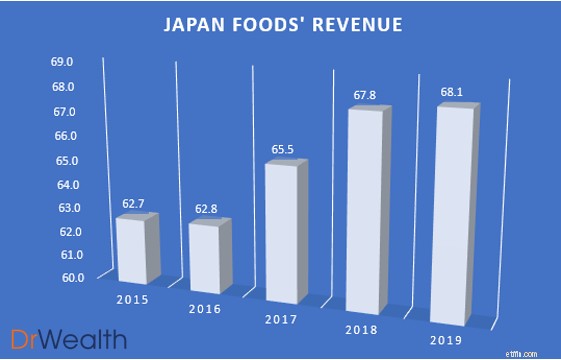

As seen in the chart, Japan Foods’ revenue has been growing year on year, albeit not substantially from 2018 to 2019. However, we would expect the top line to grow with the growth potential lined up for Japan Foods.

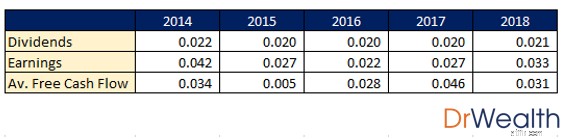

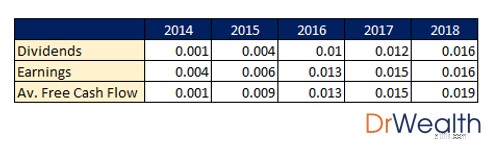

Japan Foods has been distributing consistent dividends for the past 5 years and its earnings and free cash flow has been more than the dividends distributed for all 5 years.

Similar to Jumbo, Japan Foods business growth model focuses on three things:

Japan Foods’ approach moving forward seems logical and sound. Their joint venture under the franchise “Dining Collective” is a great leap forward in their overseas ambitions, allowing them to unlock a larger customer pool by expanding their outlets and having a presence in foreign markets.

They also managed to secure and launch a new franchised ramen brand “Konjiki Hototogisu”, known for its clam-flavoured broth. The restaurant chain also has One Michelin Star.

They have since opened four restaurants under this brand in Singapore, with the latest one being launched in Jewel Changi.

This is definitely not a form of diworseification as Japan Foods aims to tackle the premium market in Singapore whilst maintaining more affordable brands for the general crowd. This caters to the tastes and wallets of the consumers, unlocking more potential for growth.

Lastly, they launched two brand extensions of “Ajisen Ramen”, named “Den by Ajisen Ramen” and “Kara-Men”.

By refreshing and rejuvenating brands, it allows Japan Foods to remain competitive and relevant in the market. To date, the response to the two variations has indeed been well with an increase in same-store sales following the rebranding.

It’s got a Niche

Lynch found that if a company focused on a particular niche, it often had little competition. Japan Foods is one of the leading F&B groups in Singapore specializing in Japanese cuisine. With 19 Dining Brands under their name and 50 locations islandwide, it seems that their restaurant network is stable and well-built.

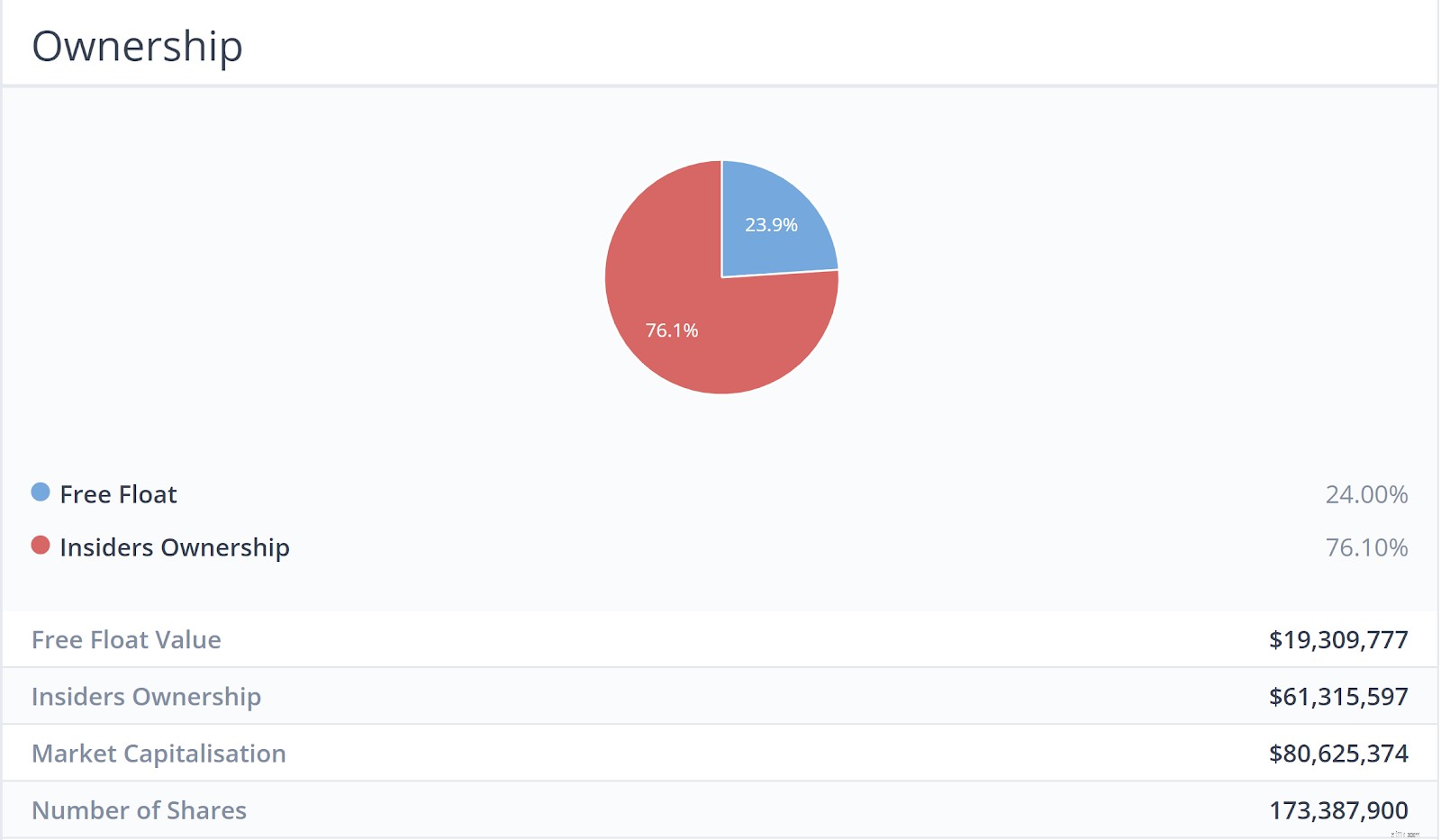

Skin in the Game (Insiders are buying/owning shares)

As can be seen, insiders of the company owned a majority of the shareholder-ship. Therefore, it proves that the management has skin in the game.

The Company is buying back shares

Japan Foods has also been posting notices in Aug 2018, Sep 2018, Dec 2018 and Feb 2018 on its daily share buybacks. Such notices can either be found on the SGX website or their investor relations website.

| Market Cap. | $186M |

| Historical Dividend Yield | 6.12% |

| Not in Sunset Industry | Yes |

| PE Ratio | 21.53 |

| Industry Average PE ratio | 47.95 |

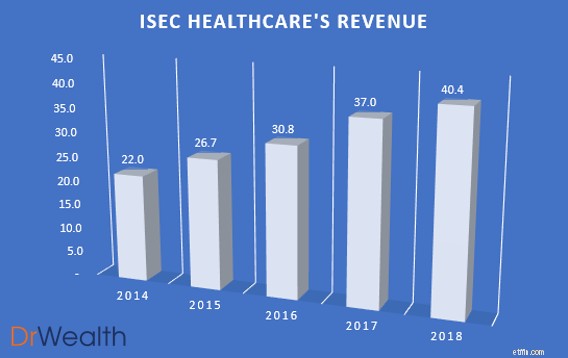

As seen in the chart, ISEC’s revenue has been growing year on year with a 9.19% growth from $37m in 2017 to $40.4M in 2018. We would also potentially expect the revenue growth to increase due to the region’s aging population and increasing awareness towards seeking early treatment for ophthalmology issues will continue to drive demand and sales upwards.

ISEC Healthcare has been distributing consistent increasing dividends for the past 5 years and its earnings and free cash flow has been more than or equal to the dividends distributed for all years.

We see growth potential in ISEC Healthcare’s business due to 3 key reasons:

Due to ageing populations, requirements for eye health care will increase. This is because there are higher incidences of Cataract, Glaucoma, Age Macular Degeneration, Dry Eyes and Vitreoretinal.

Furthermore, not only is government spending on healthcare services increasing across the region in line with changes in demographics, rising income levels and subsequent private insurance coverages has led to an increase in individual spending on private eye-care services.

ISEC Healthcare is also keen on regional expansions with large populations. They took a positive step towards this direction by announcing the incorporation of ISEC MYANMAR. They are also keen on leveraging upon the aforementioned trends to continue pursuing investment opportunities and explore up-and-coming markets such as China, Indonesia and Vietnam.

It’s got a Niche

In terms of devising a business strategy, a niche company can remain focused on its area of specialization. Over time, a niche company can develop a reputation for its work in a given field. This reputation allows a niche company to position itself as a leader and expert in the field. Niche companies focus on doing one thing well rather than doing many things only adequately. ISEC Healthcare definitely has an Eye Specialist Niche. This gives it better margins as a specialist clinic than a generalist.

Skin in the Game (Insiders are buying/owning shares)

As can be seen, insiders of the company owned a majority of the shareholder-ship. Therefore, it proves that the management has skin in the game.

Not many Institutions own it

Peter Lynch states that if you find a stock with little or no institutional ownership, you’ve found a potential winner. Such companies have not been discovered by the smart money, giving it an extra potential upside.

So there you have it. The Stalwart Category explained in accordance with Peter Lynch’s guidebook.

Lynch expected stalwarts to deliver gains of 30% to 50%, after which he would sell them and find new, undervalued counters. These are the stocks that he would frequently replace with others in this category.

Next, we’re going in-depth into one of the six different categories pointed out by Lynch – The Fast Growers

These counters are among Lynch’s favourite investment. These stocks typically have the characteristics of small, aggressive new enterprises that grow at 20-25% a year. Lynch claims that if you were to choose these Fast Growers correctly, it could potentially be a 10 to 40 bagger.

We would be picking stocks utilizing the following criteria to select our Top 3 Fast Growers:

To elaborate a little further on the above criteria:

At Dr Wealth, we believe that the Singapore Stock Exchange Market is more catered towards investors with the strategy of earning a passive income. Thus, while SGX is a fantastic market for dividend stocks/REITs there are much better growth stocks available beyond SGX.

We would, therefore, apply the aforementioned criteria in the US markets as we feel that growth stocks are aplenty there.

Given the above criteria, we shortlisted 3 Fast Growers that we will cover today, which we feel have significant growth potential. In addition, all of the stocks will have one or more of the following traits of a ten-bagger, representing a potential return 10X of what you invested.

| Market Cap. | $11.62B |

| Debt-to-Equity Ratio | 18.54 |

| Stable Top &Bottom Line Y-O-Y | Yes |

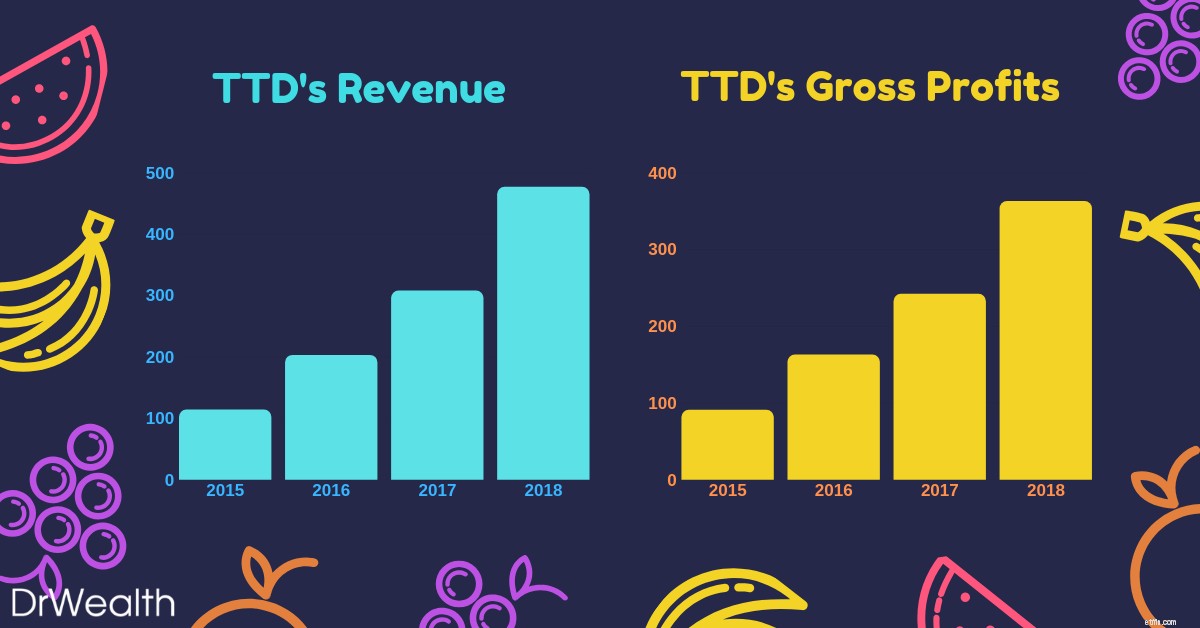

As seen in the graph, The Trade Desk’s earnings have been growing year-on-year from 2015 to 2018. Earnings grew from $242M in 2017 to $363M in 2018, displaying a whopping 50.1% growth versus the prior year.

We would also potentially expect the earnings growth to maintain or even increase as The Trade Desk looks towards gaining a firmer foothold in China and other regions.

What does The Trade Desk do?

Do you realize that what you have searched on Google would start popping up in your Facebook/Instagram/Youtube feeds as adverts?

Eerily, most of the adverts are also very relevant to what you are interested in. Welcome to the world of Programmatic Advertising!

The Trade Desk is essentially a programmatic advertising company which operates a cloud-based platform that lets companies streamline their efforts to the apt consumer’s groups they are targeting.

This, in turn, cuts down the advertising expenditure of the company and allows it to achieve a greater ROI with its adverts.

TTD allows its customers to buy targeted ad space on many different channels like social media, video/streaming, audio and many more.

The Trade Desk’s Growth Potential

Jeff Green, chief executive officer and founder of The Trade Desk, sees China as an untapped market.

This strategic move was solidified with its launch in China earlier this year, inking deals with tech powerhouses such as Alibaba, Baidu and Tencent.

Thus far, companies such as Sheraton Hotels have successfully utilized the platform to expand their customer base greatly through its targeted advertisements.

In the next five years, CEO Jeff Green claims that The Trade Desk plans to turn China into one of its top three markets.

The company says international revenue currently accounts for about 15% in revenue but expects it to grow to roughly two-thirds of its total revenue as the programmatic industry matures.

For investors, this means that there is still huge untapped potential for The Trade Desk to grow as it would take awhile for one to see material contributions from the China market to its top &bottom lines.

With the company already growing at such a blistering pace Y-O-Y without tapping on China, one would potentially expect their growth to sustain or even increase in the future.

With earnings growth, this would inevitably lead to greater appreciation in stock prices, thus allowing the investor to potentially attain a multi-bagger.

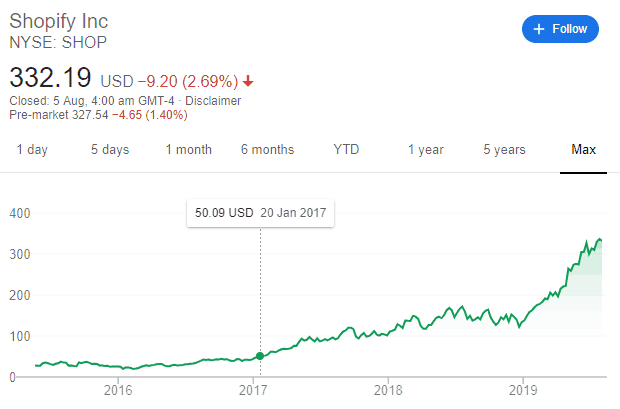

| Market Cap. | $37.38B |

| Debt-to-Equity Ratio | 5.3 |

| Stable Top &Bottom Line Y-O-Y | Yes |

As seen in the graph, Shopify’s earnings have been growing year-on-year from 2015 to 2018. Earnings grew from $380M in 2017 to $596M in 2018, displaying a huge 56.8% growth versus the prior year.

Shopify has secured its status as the e-commerce platform of choice for small entrepreneurs. Its client base and gross merchandise volume are both growing explosively.

As of June 2019, there are 820,000 Merchants from Shopify growing 55% from the prior year.

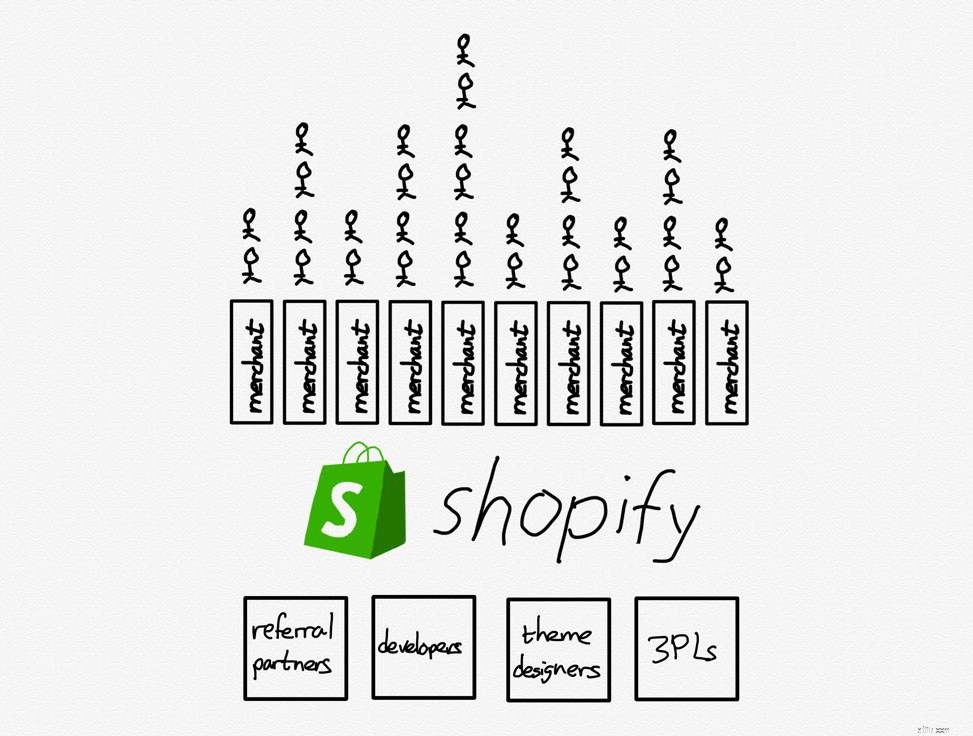

What does Shopify do?

Shopify is an e-commerce platform that allows merchants of all sizes to “set up” their own stores online. They all provide a suite of advantages such as fulfilment, payment and shipping services.

Shopify’s winning formula includes its platform’s ability to give online merchants an easy way to handle many aspects of their business:inventory management, fulfilling orders, processing payments, and communicating with current and prospective customers alike.

It is also extremely flexible with its ability to be connected with sites such as Ebay and social media such as Instagram. Small and medium-sized businesses still make up the core of Shopify’s clientele.

However, the company also offers a $2,000 a month Shopify Plus package for bigger businesses which the likes of Nestle and Red Bull utilize.

Shopify’s Growth Potential

The company estimates that there are 46 million small and mid-sized businesses around the world, and it’s only serving 1.3% of them. That leaves plenty of opportunities for Shopify to keep growing well into the future.

With the advent of the switch from traditional/physical shopping to online commerce, Shopify’s addressable market continues to grow as e-commerce captures a larger share of overall shopping.

Furthermore, one should note that Shopify isn’t a competitor to Amazon.

Amazon is an aggregator who internalises suppliers (people think they buy from amazon but actually make purchases from other suppliers).

Shopify as a platform externalises suppliers (people buy from various brands without knowing shopify powers them). There is nothing to purchase on Shopify.com other than its suite of platforms, unlike Amazon.

TLDR, Amazon is pursuing customers and bringing suppliers and merchants onto its platform on its own terms. Shopify is giving merchants an opportunity to differentiate themselves while bearing no risk if they fail.

The only way to beat an aggregator is to be a platform that externalise suppliers with differentiation.

For investors, this is a great business model which is still helmed by its charismatic and visionary founder, Tobi Lutke. In the long run, Shopify could potentially continue dominating the market and growing at a blistering pace.

With a huge untapped addressable consumer market and large growth capacities, Shopify as a fast grower could turn into one of the legendary Lynch Multi-Baggers.

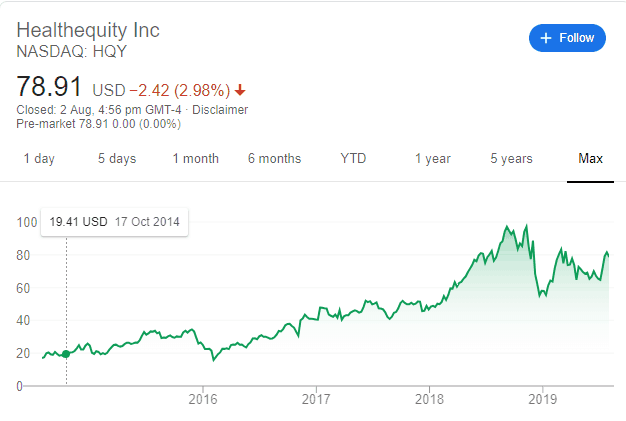

| Market Cap. | $4.95B |

| Debt-to-Equity Ratio | 7.56 |

| Stable Top &Bottom Line Y-O-Y | Yes |

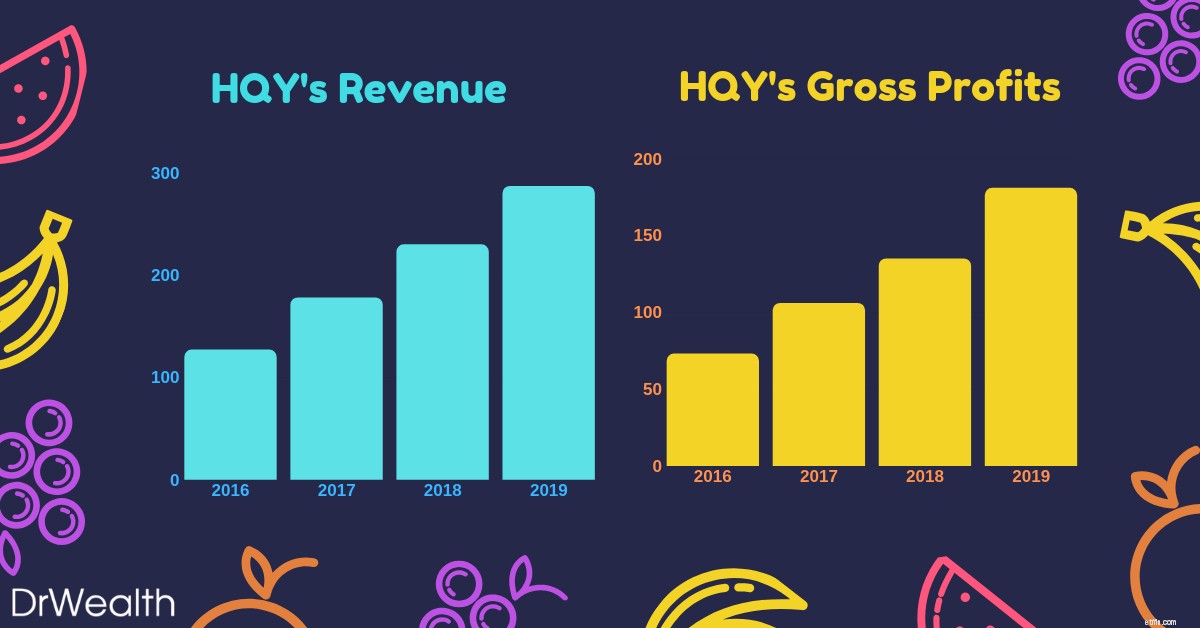

As seen in the graph, Health Equity’s earnings have been growing year-on-year from 2016 to 2019. Earnings grew from $135M in 2018 to $181M in 2019, displaying a 34% growth versus the prior year.

HealthEquity is not only profitable but has also seen impressive profit growth to go with rising sales in recent years.It’s identified multiple pathways toward future expansion that includes both organic growth and potential strategic transactions.

What does Health Equity do?

Health Equity is a cloud-based platform that provides access to Health Savings Accounts (HSAs) and other health-care benefits.

HSAs were implemented by the US Federal Government in 2003. It allows one to set aside cash for certain healthcare expenses that are not covered by their insurance.

HSAs come with huge tax benefits:money placed inside of HSAs are tax-deductible, and investments inside the HSA grow on a tax-deferred basis.

Additionally, withdrawals from HSAs aren’t taxed as long as the money is used to cover qualified healthcare expenses.

They help employers and employees alike to save on healthcare costs while taking advantage of tax incentives provided.

Health Equity’s growth potential

Health Equity’s business model is also simple:

With recurring revenue and simple services, Health Equity is definitely in it for the long run.

Furthermore, its founder, Stephen Neeleman was one of the doctors that lobbied for the federal government to implement HSAs and then subsequently built the platform, Health Equity to trade the accounts.

Rising Health Care costs will definitely be a huge proponent that drives up the demand for Health Equity services and products.

As the number of discerning healthcare consumers expands exponentially, interest in Health Savings accounts and highly deductible savings plans will rise in tandem.

For investors, the rising number of consumers being aware of Health Savings Accounts will drive demand for Health Equity’s platform. This would subsequently propel top-line sales and in turn, earnings.

With Earnings growth comes appreciation in stock prices.

So there you have it. The Fast Growers Category explained in accordance with Peter Lynch’s guidebook. If you choose wisely, this is the land of the 10-40 baggers and even the 200 baggers. However, Lynch reminds us that there’s plenty of risk in fast growers, especially in the younger companies that tend to be overzealous and underfinanced.

The stock market also does not look too kindly fast growers that run out of steam and turn in to slow growers. Hence, it is essential to figure out when the company is going to stop growing (lack of future plans, depreciating financials and loss of key leadership).

As one would notice, Peter Lynch identifies a stock using Qualitative Analysis before diving into the Quantitative.

That means he looks at a stock’s story before he looks at a stock’s business. There is nothing inherently wrong with that.

Whether you approach it from the numbers angle or the story, both ways work. However, we would advise retail investors to focus on approaching stock investing from the quantitative side of things.

This is to avoid biases and to avoid falling in love with a stock’s story. To hunt growth stocks, we have developed a robust, evidence-based framework that has delivered stellar returns per year historically. You can join us at a live session to learn more.

Next, we would be going in-depth into one of the six different categories pointed out by Lynch – The Asset Plays

Asset Plays are stocks that are believed by investors to be undervalued because the current price does not reflect the current value of the company’s assets displayed on its balance sheet.

The rationale for purchasing the stock is that the company’s assets are being offered to the market relatively cheaply, making it attractive to investors.

It would be sort of like buying a house for $0.40 on the $1.

Investors who utilize this strategy believe that the market overreacts, resulting in stock price movements that do not correspond with a company’s long-term fundamentals, giving an opportunity to profit when the price is deflated.

In fact, here at Dr Wealth, we employ our Conservative Net Asset Valuation (CNAV) method to identify to evaluate and select deeply undervalued Asset Plays.

We provide “Skin in the Game” case studies of our winning stocks that were hand-picked using our proprietary CNAV screener, substantiating them with past transaction statements.

We would thus be picking stocks utilizing the following criteria to select our Top 3 Asset Plays:

To elaborate a little further on the above criteria:

This is the formula we use to calculate a stock’s Conservative Net Asset Value:

All of which can be found in the Balance Sheet of the company’s financial statements.

We would then take the CNAV2 value, divided by total shares outstanding to find the CNAV2 per-share value .

Thus, if the CNAV2 per-share value is HIGHER than that of the current price per share, it is deemed to be on a discount.

To make our selection more stringent, we turn to Dr Joseph Piotroski’s F-score to find fundamentally strong low price-to-book stocks that are worth investing in.

As we have already added conservativeness, we do not need to adopt the full 9-point F-score. A proxy 3-point system known as POF score would be used instead.

It stands for Profitability , Operating Efficiency and Financial Position .

The stocks selected has to have a POF score of 2 and above.

To learn more about the POF score and how we use it in our investment strategies, click here.

An easy way to bypass such subjective questions is to look at whether management owns the majority of the shares in the company.

Today, we would be looking at the Hong Kong Stock Exchange market due to the recent correction caused by the protests. This resulted in many counters being ‘On-Sale’ even though its fundamentals have not faced any drastic changes.

To facilitate your reading, we have structured the content into clear and concise points to sum up what you have to know:

While there isn’t a hard and fast exit strategy, at Dr Wealth we would either sell at the 3 year holding period , when the Financial Fundamentals change or when a key qualitative point has been changed (i.e. change of CEO/founder steps down).

| Market Cap. | $1.173B |

| Market Price | $0.173HKD |

| CNAV2 Value per share | $0.386HKD |

| Net Asset Value per share | $0.659HKD |

| POF score | 3 |

| Potential Profit | 281% |

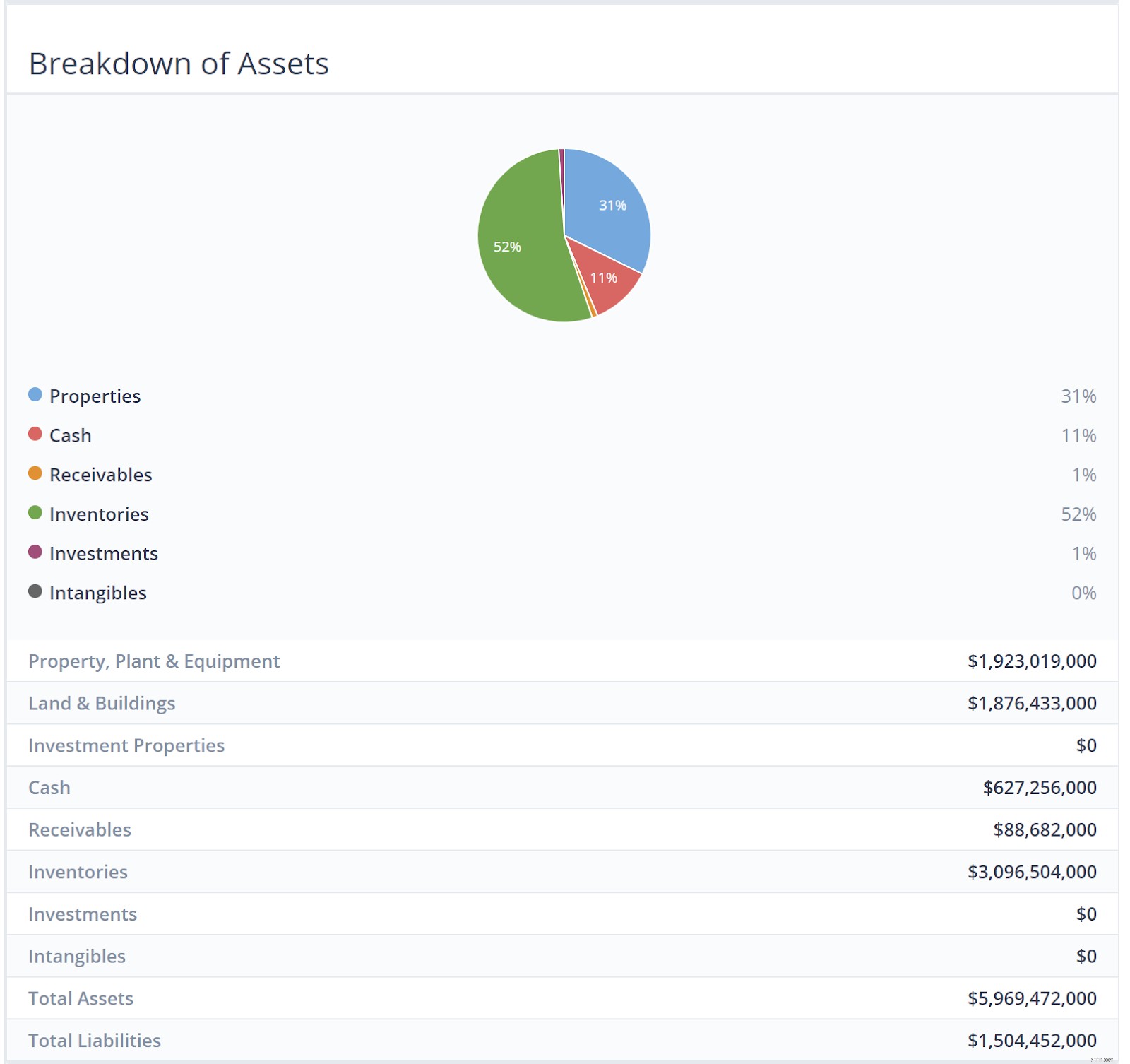

Emperor Watch &Jewellery is a retailer of European-made internationally renowned watches such as Patek Philippe, Rolex and Tudor. This is coupled with the sales of self-designed fine jewellery under its own brand, ‘Emperor Jewellery’.

The company has a history of over 75 years, establishing over 90 stores across Hong Kong, Macau, mainland China, Singapore and Malaysia, as well as an online shopping platform, and now has over 1,100 staff.

As seen in the infographic above, Inventories and Properties make up the bulk of their assets. There is a whopping HK$3.09 billion worth of luxury watches and Jewellery.

My hypothesis was that it wouldn’t be that bad because luxury watches and jewellery retain value pretty well as long as they are not worn and still in good condition.

We went ahead to discount the current inventory of watches and jewellery at 50%. We should account for a large margin of safety when calculating the valuation of Emperor Watch &Jewellery.

The Company’s core strategy focuses on maintaining its position as the leading watch and jewellery retailing group in Greater China, coupled with an eye on expansion beyond the region.

As most of their customers are mainlanders, boutique stores that peddled luxury goods such as watches and jewellery enjoyed the patronage of this swell of new customers as a result.

However, most of this all came to a halt when President Xi Jing Ping decided to rein in on the corruption.

This discouraged ostentatious displays of wealth in public. Sales of luxury goods to Chinese consumers slowed for a time and as earnings dropped, so did share prices.

Coupled with the recent 10 straight weeks of anti-government protests in Hong Kong, stock prices in the HK Exchange have inevitably taken a massive beating. This is without even mentioning the massive backdrop created by the Trump-China trade war affecting prices as well!

More than $600 billion of stock market value has been erased since early July thanks to the riots and protests.

The culmination of all these events have thus done something favourable for us; create opportunities for us to businesses at fantastic bargain prices.

| Market Cap. | $97.101B |

| Market Price | $47.4HKD |

| CNAV2 Value per share | $68.357HKD |

| Net Asset Value per share | $105.846HKD |

| POF score | 3 |

| Potential Profit | 121% |

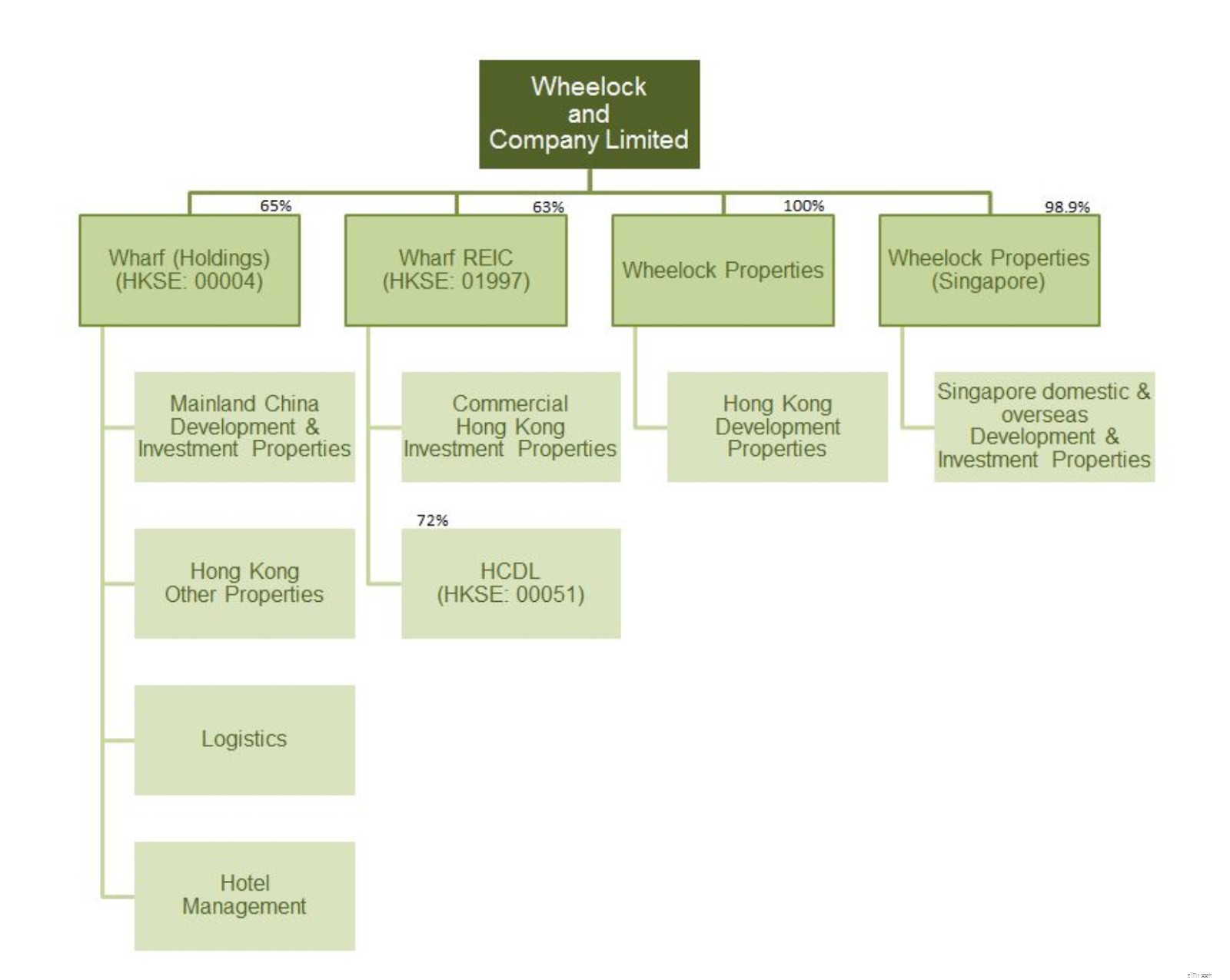

Wheelock &Co. is principally engaged in property development in Hong Kong, and in property investment and development in Singapore.

Their major subsidiaries include Wharf (Holdings) Limited (HKSE:00004), Wharf REIC Limited (HKSE:01997), Wheelock Properties Limited and Wheelock Properties (Singapore) Limited.

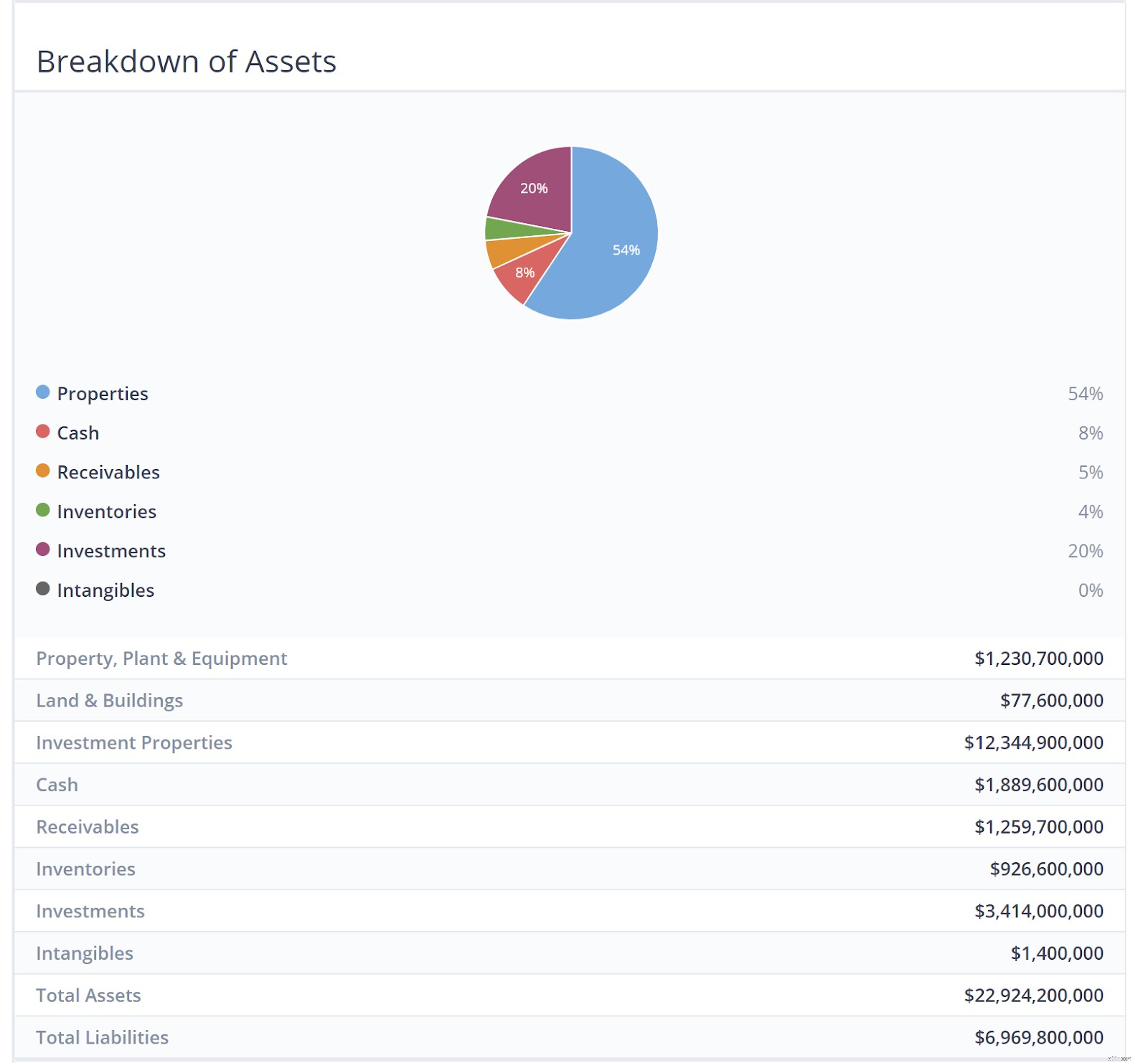

As seen in the infographic above, Properties make up the bulk of their assets. This should be rightfully so as they are engaged in the property development business.

Due to the sheer amount of properties available in the company, we would only touch on the assets of Wheelock Properties here.

Kindly refer to the company’s website should you like to find out more about its other major subsidiaries asset breakdown.

| Market Cap. | $2.48B |

| Market Price | $4.69HKD |

| CNAV2 Value per share | $15.067HKD |

| Net Asset Value per share | $24.966HKD |

| POF score | 3 |

| Potential Profit | 420% |

The Group is a Hong Kong-based property developer focusing on investing and developing property projects in Mainland China and aims to develop high-quality products to create sustainable value for its shareholders.

The Group has a diversified property portfolio model with investments in both residential projects for sale and commercial projects mainly for rental income.

The group is organized into 3 main operating segments:

Over the long term, the Group seeks to maintain a balance between residential development for sale and commercial investment properties for lease in order to create a sustainable model with growth potential.

Residential properties for sale generate fast turnover, which should enhance return on equity. Investment properties for lease, on the other hand, create steady recurring income and cash flow as well as long term capital appreciation and are relatively immune from the periodic restrictions on residential properties.

The Group has also made an investment in the renewable energy sector and believes shareholders may benefit from China’s need to develop non-polluting sources of energy.

As seen in the infographic above, similar to Wheelock &Co, Properties make up the bulk of their assets. This should be rightfully so once again as they are engaged in the property development business.

The assets are mostly located around the more developed, coastal regions of China – where population density and income levels are much higher.

This could largely be attributed to the slowdown of the Chinese property sector in 2018. China’s massive property market is expected to cool further in 2019, with smaller price rises and falling home sales adding to pressure on the world’s second-largest economy, a Reuters poll showed.

As a result, residential sales volume began declining in the second half of 2018, with declines of 1% year on year in September and October and 4% in November. It increased by 2.5% in December, but poor Chinese New Year’s data suggest that the decline will continue into 2019.

Moreover, the price rise growth for new residential properties has decelerated for the third straight month. In January, residential prices for 70 major cities increased by only 0.61% compared to December, the slowest pace in nine months.