লেখক:জেফরি লেভিন, CPA/PFS, CFP®, AIF, CWS®, MSA টিম কিটস

Jeffrey Levine, CPA/PFS, CFP, AIF, CWS, MSA হল Kitces.com-এর লিড ফিনান্সিয়াল প্ল্যানিং নের্ড, আর্থিক পরিকল্পনা পেশাদারদের জন্য একটি শীর্ষস্থানীয় অনলাইন সংস্থান, এবং এছাড়াও তিনি বাকিংহাম ওয়েলথ পার্টনারদের প্রধান পরিকল্পনা কর্মকর্তা হিসেবে কাজ করেন। 2020 সালে, অনিশ্চিত সময়ে ফিরে আসার জন্য শীর্ষ 25টি কণ্ঠের মধ্যে একটি হিসাবে জেফ্রির নাম বিনিয়োগ উপদেষ্টা ম্যাগাজিনের IA25-এ নামকরণ করা হয়েছিল। এছাড়াও 2020 সালে, জেফ্রিকে আর্থিক উপদেষ্টা ম্যাগাজিন দ্বারা ওয়াচের তরুণ উপদেষ্টা হিসাবে নামকরণ করা হয়েছিল। জেফরি হলেন স্ট্যান্ডিং ওভেশন অ্যাওয়ার্ডের একজন প্রাপক, যা "ব্যক্তিগত আর্থিক পরিকল্পনা পরিষেবাগুলিতে অনুকরণীয় পেশাদার অর্জন" এর জন্য AICPA আর্থিক পরিকল্পনা বিভাগ দ্বারা উপস্থাপিত হয়েছে। InvestmentNews দ্বারা 40 অনূর্ধ্ব 40-এর 2017 শ্রেণীতেও তাকে নাম দেওয়া হয়েছিল, যা "কৃতিত্ব, আর্থিক পরামর্শ শিল্পে অবদান, নেতৃত্ব এবং ভবিষ্যতের প্রতিশ্রুতি" স্বীকৃতি দেয়। জেফরি হলেন স্যাভি আইআরএ প্ল্যানিং®-এর স্রষ্টা এবং প্রোগ্রাম লিডার, সেইসাথে স্যাভি ট্যাক্স প্ল্যানিং®-এর সহ-নির্মাতা এবং সহ-প্রোগ্রাম লিডার, উভয়ই হর্সমাউথ, এলএলসি-এর মাধ্যমে দেওয়া হয়। তিনি Forbes.com, সেইসাথে অসংখ্য শিল্প প্রকাশনাতে নিয়মিত অবদানকারী এবং সাধারণত সাংবাদিকরা তার অন্তর্দৃষ্টির জন্য খোঁজ করেন। আপনি Twitter @CPAPlanner-এ জেফকে অনুসরণ করতে পারেন

জেফের আরও নিবন্ধ এখানে পড়ুন।

22 জানুয়ারী, 2020-এ, সেন্টার ফর ডিজিজ কন্ট্রোল অ্যান্ড প্রিভেনশন (CDC) মার্কিন যুক্তরাষ্ট্রে পরীক্ষাগার-নিশ্চিত COVID-19-এর প্রথম মামলার বিজ্ঞপ্তি পেয়েছে। পরের দিন, সপ্তাহ এবং মাসগুলিতে ভাইরাসটি মার্কিন যুক্তরাষ্ট্র জুড়ে ছড়িয়ে পড়তে থাকে, যার ফলে একটি স্বাস্থ্য সংকট দেখা দেয় যার ফলে আজ পর্যন্ত প্রায় এক মিলিয়ন আমেরিকান প্রাণ হারিয়েছে।

দুর্ভাগ্যবশত, এটি শুধুমাত্র মার্কিন ইতিহাসের সবচেয়ে খারাপ মহামারীগুলির মধ্যে একটি কীভাবে আমেরিকানদের প্রভাবিত করেছে তার গল্প বলতে শুরু করে। প্রাণহানির মর্মান্তিক ক্ষতির পাশাপাশি, কোভিড-১৯ মহামারীটি মার্কিন অর্থনীতিতেও বিপর্যয় সৃষ্টি করেছে। ঋতুগতভাবে সামঞ্জস্য করা বেকারত্ব প্রায় রাতারাতি 4% থেকে প্রায় 15%-এ বেড়েছে, কারণ 20 মিলিয়নেরও বেশি আমেরিকান শুধুমাত্র এপ্রিল 2020 সালে বেকারত্বের সুবিধার জন্য আবেদন করেছে।

20-মিলিয়ন সংখ্যা হিসাবে অবিশ্বাস্য, এটি আরও খারাপ হতে পারে। উল্লেখযোগ্যভাবে, 27 মার্চ, 2020-এ, রাষ্ট্রপতি ট্রাম্প কর্তৃক 2020 সালের করোনভাইরাস এইড, ত্রাণ এবং অর্থনৈতিক নিরাপত্তা (CARES) আইনে স্বাক্ষর করা হয়েছিল। কেয়ারস অ্যাক্ট ছিল $2 ট্রিলিয়ন-এরও বেশি ত্রাণ প্যাকেজ এবং পেচেক প্রোটেকশন প্রোগ্রামের (পিপিপি) জন্য $349 বিলিয়ন বরাদ্দ (যা শেষ পর্যন্ত পেচেক প্রোটেকশন প্রোগ্রাম এবং হেলথ কেয়ার এনহ্যান্সমেন্ট অ্যাক্ট দ্বারা মোট $659 বিলিয়নে বৃদ্ধি করা হয়েছিল) অন্তর্ভুক্ত ছিল, ক্ষুদ্র ব্যবসায় সংগ্রামের জন্য একটি নতুন ধরনের ঋণ যা ক্ষুদ্র ব্যবসা প্রশাসনের দ্বারা সম্পূর্ণরূপে নিশ্চিত করা হবে।

এই PPP ঋণগুলি অনেক ছোট ব্যবসার মালিকদের শুধুমাত্র COVID-19 মহামারীর শুরুতে টিকে থাকতেই সাহায্য করেনি বরং তাদের কর্মচারীদের চাকরিও সংরক্ষণ করতে সাহায্য করেছিল। লোনগুলি ন্যূনতম আন্ডাররাইটিং, মাত্র 1% সুদের হার এবং 2 থেকে 5 বছরের মধ্যে মেয়াদপূর্তির সাথে এসেছে (5 জুন, 2020-এ বা তার পরে অর্থায়ন করা ঋণের মেয়াদ 5 বছর এবং লোনগুলি 5 জুন, 2020-এর আগে অর্থায়ন করা হয়েছে , 2 বছরের পরিপক্কতা আছে, যদি না ঋণগ্রহীতা এবং ঋণদাতা পারস্পরিকভাবে একটি এক্সটেনশনে সম্মত হন।

কিন্তু ঋণের শর্তাবলী আকর্ষণীয় হলেও, শীর্ষে থাকা চেরি - ব্যবসার মালিকদের জন্য বড় সুবিধা যা তাদের লোন নেওয়ার জন্য যথেষ্ট প্রলুব্ধ করার জন্য ছিল। প্রথম স্থানে - নিঃসন্দেহে কিছু (বা সম্ভাব্য সব) ঋণ মাফ করা করার ক্ষমতা ছিল , যা কার্যকরভাবে ঋণকে 'বিনামূল্যে' অর্থের অনুদানে পরিণত করবে।

তবে, পিপিপি ঋণের ক্ষমা স্বয়ংক্রিয় নয়। পরিবর্তে, অনেক ক্ষেত্রে, ব্যবসার মালিকরা এখন যে পছন্দ এবং সিদ্ধান্তগুলি গ্রহণ করে, এমনকি ঋণ পাওয়ার কয়েক মাস পরেও, তাদের ঋণের কতটা মাফ হবে তাতে গুরুত্বপূর্ণ ভূমিকা পালন করতে পারে। তদনুসারে, উপদেষ্টাদের পিপিপি ঋণ ক্ষমার নিয়মগুলি বোঝা উচিত, যাতে তারা প্রক্রিয়াটির মাধ্যমে ছোট ব্যবসার মালিকদের গাইড করতে সহায়তা করতে পারে৷

পেচেক প্রোটেকশন প্রোগ্রাম (PPP) এক নজরে

পিপিপি ছিল ভয়ঙ্কর গতিতে ছোট ব্যবসার মালিকদের হাতে অর্থ পাওয়ার একটি অভূতপূর্ব প্রচেষ্টা, যা সারা দেশে অবিশ্বাস্যভাবে বিশাল পরিমাণে ছোট ব্যবসার অস্তিত্বের কারণে কোন ছোট কৃতিত্ব নয়। এটি করার জন্য, পিপিপি ব্যাংক, ক্রেডিট ইউনিয়ন এবং অন্যান্য অনুমোদিত ঋণদাতাদের উপর নির্ভর করে ঋণের আন্ডাররাইট এবং প্রক্রিয়াকরণের জন্য, যা SBA দ্বারা সম্পূর্ণরূপে সমর্থিত হবে (সম্ভাব্য-সঙ্কট-সঙ্কটে ছোটদের অর্থ ঋণ দেওয়ার ক্ষেত্রে সেই ঋণদাতাদের ঝুঁকি দূর করতে ব্যবসায়িক ঋণগ্রহীতা)। সেই লক্ষ্যে, এপ্রিলের শুরু থেকে, 8 আগস্ট, 2020 তারিখে প্রোগ্রামের সমাপ্তির (অন্তত নতুন পিপিপি ঋণ প্রদানের উদ্দেশ্যে) মাধ্যমে, প্রায় 5,460টি বিভিন্ন ঋণদাতা 5,212,128টি ঋণের সুবিধা দিয়েছে!

অবিশ্বাস্যভাবে, CARES আইন থেকে PPP তহবিলের প্রথম রাউন্ড ($349 বিলিয়ন) মাত্র কয়েক সপ্তাহের মধ্যে চলে গেছে, কারণ SBA 16 এপ্রিল, 2020-এ PPP আবেদনগুলি গ্রহণ করা বন্ধ করে দেয়, আইনে স্বাক্ষর হওয়ার তিন সপ্তাহেরও কম সময় পরে। দ্বিতীয় রাউন্ডের তহবিল, যা এই প্রোগ্রামে অতিরিক্ত $310 বিলিয়ন যোগ করেছে, পেচেক প্রোটেকশন প্রোগ্রাম এবং হেলথ কেয়ার এনহ্যান্সমেন্ট অ্যাক্টের অংশ হিসাবে, 24 এপ্রিল, 2020 থেকে উপলব্ধ হয়েছে৷

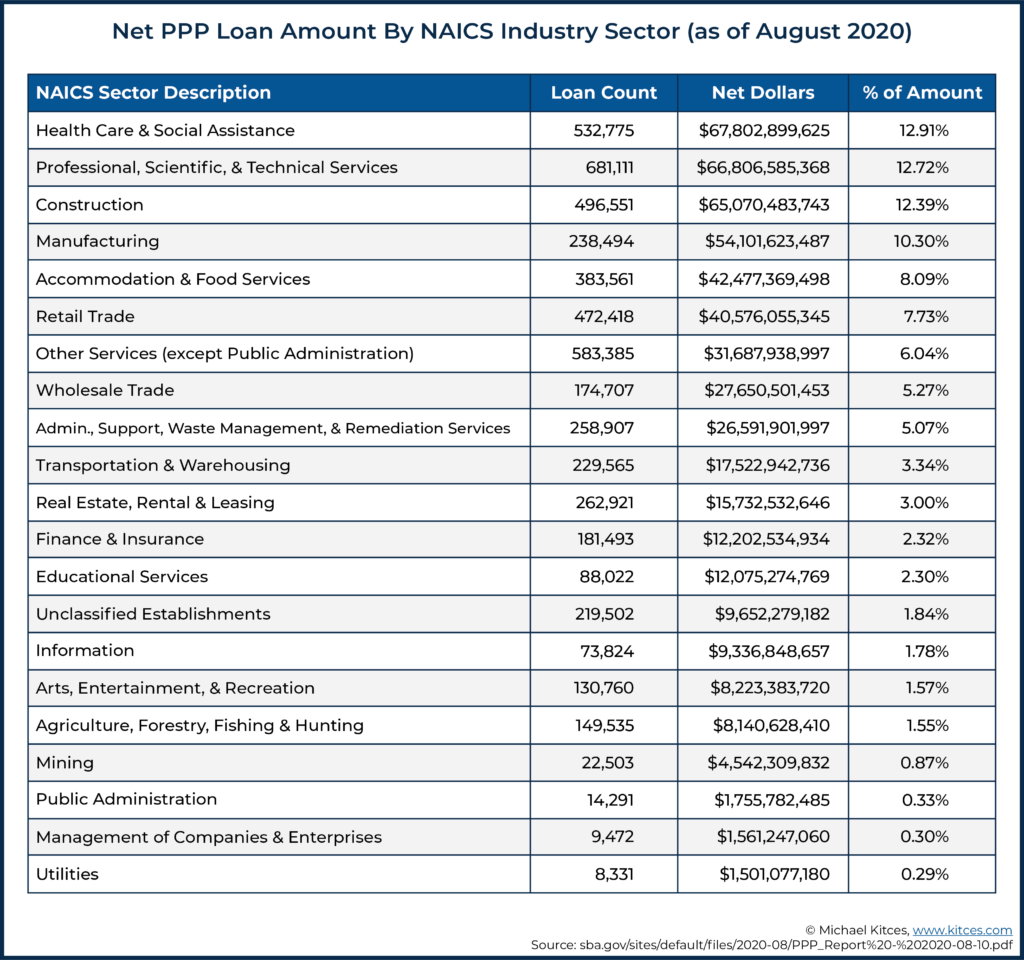

শেষ পর্যন্ত, অতিরিক্ত তহবিল যথেষ্ট থেকে বেশি প্রমাণিত হয়েছে। 8 অগাস্ট, 2020-এ প্রোগ্রামের শেষ তারিখ অনুসারে, PPP প্রোগ্রামের (অর্থাৎ, শেষ পর্যন্ত, $349 + $310 =$134 বিলিয়ন) প্রায় প্রতিটি ধরণের ব্যবসার জন্য প্রায় $525 বিলিয়ন ঋণ অনুমোদন করা হয়েছিল (নীচের চার্ট দেখুন) $659 বিলিয়ন যা এই প্রোগ্রামে বরাদ্দ করা হয়েছিল তা অব্যবহৃত হয়েছে)।

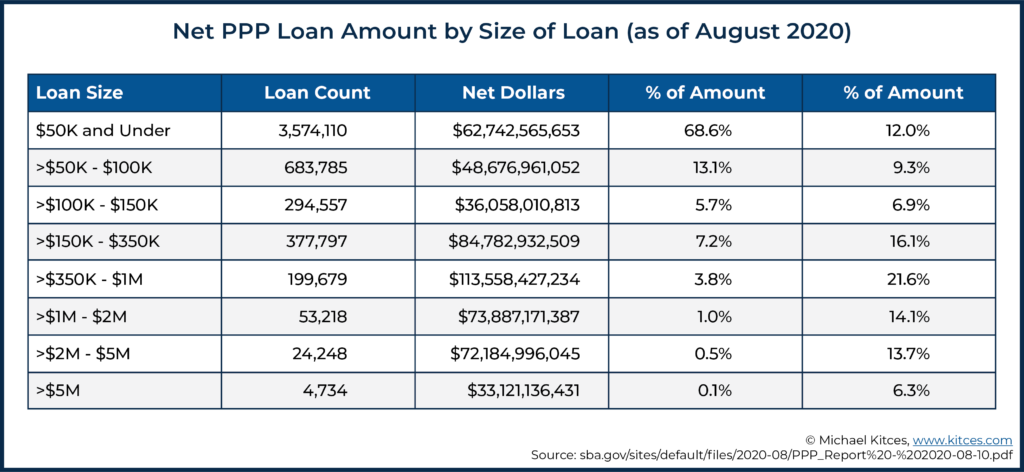

পিপিপির অধীনে ইস্যুকৃত ঋণের অধিকাংশই ছিল তুলনামূলকভাবে ছোট। প্রকৃতপক্ষে, নীচের চার্টটি চিত্রিত করে, জারি করা প্রায় 5.2 মিলিয়ন ঋণের মধ্যে, প্রায় 70% ছিল $50,000 বা তার কম ঋণের জন্য। এটি লক্ষণীয় যে, তাদের ব্যাপকতা থাকা সত্ত্বেও, এই ধরনের ঋণগুলি জারি করা সমস্ত ঋণের মোট মূল্যের 12% জন্য দায়ী (যেহেতু অনেকগুলি খুব ছোট ঋণের উচ্চ পরিমাণ এখনও তুলনামূলকভাবে অল্প পরিমাণে যোগ করে)। বিপরীতে, $5 মিলিয়ন থেকে $10 মিলিয়ন (পিপিপির অধীনে উপলব্ধ সর্বাধিক পরিমাণ) ঋণগুলি সমস্ত জারি করা ঋণের মাত্র 0.1% প্রতিনিধিত্ব করে তবে সমস্ত পিপিপি তহবিলের 6.3% জন্য দায়ী৷

পেচেক সুরক্ষা কর্মসূচির (পিপিপি) ঋণের সর্বাধিক পরিমাণ গণনা করা

PPP ঋণ ব্যবসার জন্য উপলব্ধ ছিল, যদি ব্যবসা দুটি প্রয়োজনীয়তা পূরণ করে। প্রথমত, এটিকে একটি "ছোট ব্যবসা" হিসাবে বিবেচনা করতে হয়েছিল, যা সাধারণত 500 টির কম কর্মচারীদের হিসাবে সংজ্ঞায়িত করা হয়েছিল (শিল্পের নির্দিষ্ট কিছু ব্যবসা যেখানে NAICS কোড উচ্চতর কর্মচারী আকারের মান প্রদান করে তারা যোগ্যতা অর্জন করতে সক্ষম হয়েছিল)। দ্বিতীয়ত, ব্যবসাকে একটি সৎ-বিশ্বাসের শংসাপত্র তৈরি করতে হবে যে তাদের ঋণের অনুরোধ ছিল “প্রয়োজনীয় COVID-19 এর কারণে বর্তমান অর্থনৈতিক অবস্থার অনিশ্চয়তার কারণে।"

যদি একটি ব্যবসা এই দুটি শর্ত পূরণ করে, এটি তাদের গড় "যোগ্য মাসিক বেতন" খরচের 2.5 গুণের কম, বা $10 মিলিয়নের সমান একটি পিপিপি ঋণ পাওয়ার যোগ্য ছিল৷

যোগ্য মাসিক বেতনের খরচের মধ্যে রয়েছে কর্মচারীদের বেতন এবং মজুরি, এবং একমাত্র মালিক এবং অংশীদারদের জন্য লাভ (যার প্রত্যেকটি বিবেচনা করা যেতে পারে এমন বেতন/মজুরি/আয়ের সর্বোচ্চ $100,000 বার্ষিক পরিমাণ সাপেক্ষে), সেইসাথে এর জন্য করা অর্থপ্রদান। কর্মচারীদের গ্রুপ স্বাস্থ্য সুবিধা, অবসর গ্রহণের অবদান, এবং রাজ্য এবং স্থানীয় কর।

ব্যবসার গড় মাসিক বেতন নির্ধারণের উদ্দেশ্যে, ব্যবসাগুলি সাধারণত 2019 এর জন্য গড় মাসিক বেতন ব্যবহার করে। তবে, মৌসুমী ব্যবসাগুলি 15 ফেব্রুয়ারি, 2019 এবং 30 জুন, 2019 বা যেকোনো 12-সপ্তাহের মধ্যে গড় মাসিক বেতন ব্যবহার করতে সক্ষম হয়েছিল 1 মে, 2019 এবং 15 সেপ্টেম্বর, 2019-এর মধ্যে সময়কাল। অন্যদিকে, নতুন ব্যবসাগুলি (অর্থাৎ, যেগুলির এত ঐতিহাসিক বেতন নম্বর ছিল না কারণ এটি 2019 সালে চালু ছিল না) তাদের গড় ব্যবহার করতে সক্ষম হয়েছিল 1 জানুয়ারি, 2020 থেকে 29 ফেব্রুয়ারি, 2020 পর্যন্ত মাসিক বেতন।

পেচেক প্রোটেকশন প্রোগ্রাম (PPP) ঋণের অর্থ কী ব্যয় করা যেতে পারে?

অনেক ছোট ব্যবসার মালিকদের জন্য, পেচেক প্রোটেকশন প্রোগ্রাম একটি লাইফলাইন ছিল যা তাদের কর্মচারীদের হেডকাউন্ট বা ক্ষতিপূরণ কমাতে বা কিছু ক্ষেত্রে সম্পূর্ণভাবে ব্যবসা বন্ধ করতে বাধা দেয়। কিন্তু যদিও পিপিপি ঋণ ব্যবসার মালিকদের অনেক প্রয়োজনীয় তারল্য প্রদান করেছিল, তারা কিছু স্ট্রিং সংযুক্ত করেছিল।

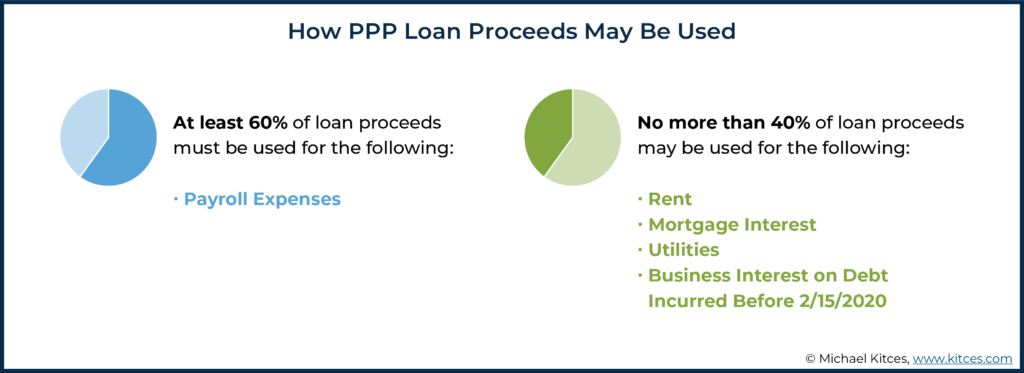

আরও সুনির্দিষ্টভাবে, CARES আইন PPP আয়ের ব্যবহার সীমিত করেছে, যার জন্য আয়ের কমপক্ষে 60% বেতনের খরচের জন্য ব্যবহার করা প্রয়োজন, এবং অবশিষ্ট অর্থ (40% এর বেশি নয়) অতিরিক্ত খরচের জন্য উপলব্ধ যা ভাড়া, বন্ধকের সুদ, ইউটিলিটি এবং অন্যান্য ব্যবসায়িক সুদ 15 ফেব্রুয়ারি, 2020 এর আগে নেওয়া ঋণের উপর।

আগেই উল্লেখ করা হয়েছে, পিপিপি ঋণ 1% সুদের হার এবং 2 বা 5 বছরের মেয়াদপূর্তিতে জারি করা হয়েছিল। সংগ্রামী ব্যবসার জন্য, সেগুলি বেশ অনুকূল শর্ত। হেক, যে কোনো এর জন্য ব্যবসা, তারা বেশ অনুকূল শর্তাবলী!

কিন্তু যখন কিছু ব্যবসা তাদের পিপিপি ঋণ ফেরত দিতে চায় (বা ইতিমধ্যেই তাদের ফেরত দিয়েছে), ব্যবসার মালিকদের সিংহভাগ যারা পিপিপি ঋণ চেয়েছিল তারা যতটা সম্ভব ঋণ মাফ করার অভিপ্রায়ে তা করেছিল।

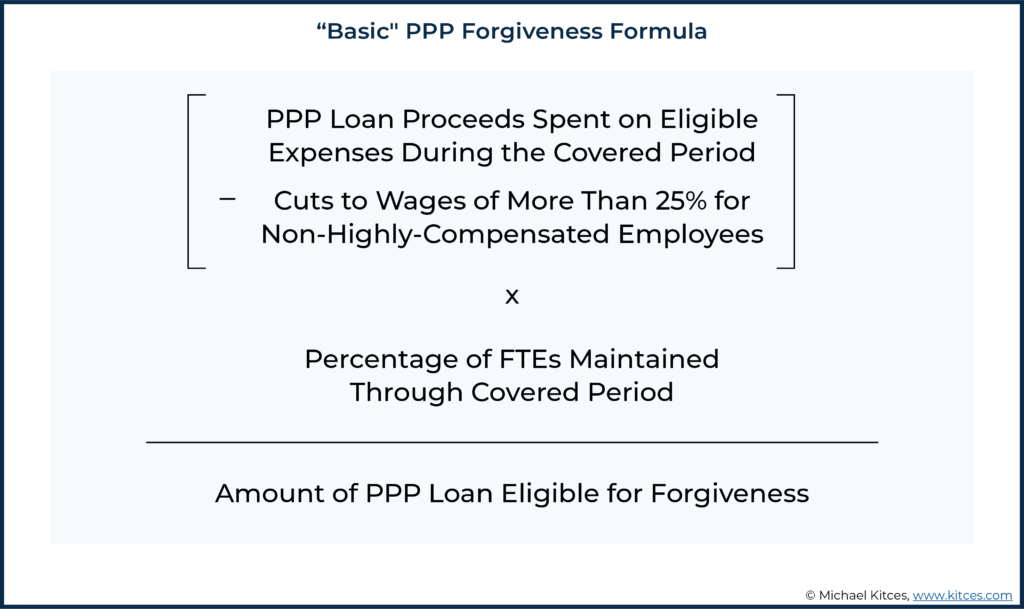

উপরিভাগে, কতটা পিপিপি ঋণ মাফ করা হবে তা নির্ধারণের সূত্রটি মোটামুটি সোজা, নীচের গ্রাফিকে চিত্রিত। অনেক নিয়ম ও প্রবিধানের মতো, তবে, 'শয়তান বিশদ বিবরণে রয়েছে', এবং কিছু পদক্ষেপের প্রয়োজন হতে পারে গণনার জন্য প্রয়োজনীয় তথ্য নির্ধারণ করার জন্য, যার মধ্যে রিপোর্ট করার কভারড পিরিয়ড, দাবি করার যোগ্য খরচ, প্রযোজ্য মজুরি হ্রাস, এবং রক্ষণাবেক্ষণ করা FTE-এর সংখ্যা।

পেচেক প্রোটেকশন প্রোগ্রাম (পিপিপি) লোনের "কভারড পিরিয়ড" বোঝা

PPP লোনের কভারড পিরিয়ড হল সেই সময়কাল যার মধ্যে ক্ষমার জন্য যোগ্য খরচগুলি "ব্যয়" হয় বা যার জন্য "পেমেন্ট করা হয়" (এক মুহূর্তের মধ্যে এটি আরও বেশি), যা ক্ষমা গণনার দিকে গণনা করতে পারে।

5 জুন, 2020 তারিখে বা তার পরে তহবিল করা ঋণের জন্য, কভারড পিরিয়ড হল সেই 24 সপ্তাহ যা লোনের আয়ের প্রাপ্তি অনুসরণ করে (অর্থাৎ, সেগুলি পাওয়ার পর 24 সপ্তাহের মধ্যে যোগ্য খরচে 'ব্যবহার' করতে হয়েছিল , ক্ষমা পাওয়ার যোগ্য হওয়ার জন্য)। বিপরীতে, যে ঋণগুলি 5 জুন, 2020-এর আগে অর্থায়ন করা হয়েছিল, মূলত তাদের কভারড পিরিয়ডের মধ্যে মাত্র 8 সপ্তাহ ছিল কিন্তু পরবর্তীতে ঋণগ্রহীতাদের কোনও একটি বেছে নেওয়ার বিচক্ষণতা দেওয়ার জন্য সংশোধন করা হয়েছিল। 8 সপ্তাহ বা 24 সপ্তাহ।

সৌভাগ্যবশত, যদিও, পিপিপি ঋণের সিংহভাগই 5 জুন, 2020-এর আগে অর্থায়ন করা হয়েছিল, এবং এইভাবে, সিংহভাগ ঋণগ্রহীতাদের 8-সপ্তাহ বা দীর্ঘ 24-সপ্তাহ (যদি প্রয়োজন হয়) কভারড পিরিয়ড বেছে নেওয়ার নমনীয়তা রয়েছে।

পেচেক সুরক্ষা প্রোগ্রাম (পিপিপি) লোনের "বিকল্প বেতনের কভারড পিরিয়ড"

স্ট্যান্ডার্ড "কভারড পিরিয়ড" ছাড়াও, SBA এবং ট্রেজারি নিয়মগুলি নিয়োগকর্তাদের একটি "বিকল্প পে-রোল কভারড পিরিয়ড" ব্যবহার করার জন্য একটি বিকল্প প্রদান করে। অল্টারনেটিভ পেরোল কভারড পিরিয়ড হল, উচ্চ স্তরে, ঠিক কীরকম শোনাচ্ছে; আরেকটি আচ্ছাদিত সময়কাল যা কিছু ব্যবসার মালিকদের দ্বারা নির্বাচিত হতে পারে যেগুলি শুধু ৷ বেতনের খরচের ক্ষেত্রে প্রযোজ্য (অন্যান্য খরচ এখনও 'নিয়মিত' কভারড পিরিয়ডের সাপেক্ষে)।

পরবর্তী শুরুর প্রথম দিনে বিকল্প বেতনের কভারড পিরিয়ড শুরু হয় পে-রোল পিরিয়ড, PPP তহবিল হওয়ার পরে (যখন একজন ঋণগ্রহীতা তাদের PPP তহবিল পেয়েছিলেন তার পরিবর্তে), এবং 8 বা 24 সপ্তাহের জন্য চলে (ব্যবসায়ের মালিকের 'নিয়মিত'-এর জন্য ব্যবহার করার জন্য যে সময়টি বেছে নেওয়া হয়েছিল/ব্যবহার করার প্রয়োজন ছিল সেই একই দৈর্ঘ্য কভার করা হয়েছে) সময়কাল)।

এটা মনে রাখা গুরুত্বপূর্ণ, যদিও, এটি সমস্ত নয় ব্যবসা এই অতিরিক্ত কভারড পিরিয়ড ব্যবহার করতে পারে। বরং, তা করার জন্য, একটি ব্যবসাকে অবশ্যই তাদের বেতন-ভাতা দ্বি-সাপ্তাহিক (বা আরও ঘন ঘন) ভিত্তিতে চালাতে হবে।

অল্টারনেটিভ পেরোল কভারড পিরিয়ড (যখন যোগ্য) ব্যবহার করার প্রাথমিক সুবিধা হল আরও বেশি বেতনের খরচ ক্ষমার জন্য গণনা করার অনুমতি দেওয়া। যেহেতু অনেক ব্যবসা আসলে একটি বেতনের মেয়াদ শেষ হওয়ার পরে কোনো সময়ে তাদের কর্মচারীদের বেতন দেয়, বিকল্প কভারড পেরোল পিরিয়ড ব্যবহার করে সেই ব্যবসাটিকে তার বিকল্প কভারড পেরোল পিরিয়ডে অন্তর্ভুক্ত পূর্ববর্তী বেতনের সময়সূচির খরচের মোট পরিমাণ পেতে দেয়।

অল্টারনেটিভ কভারড পেরোল পিরিয়ড ব্যবহার করলে দুটি আলাদা কভারড পিরিয়ডের ট্র্যাক রাখার অতিরিক্ত জটিলতা আসে (কারণ শুধু বেতনের খরচগুলি বিকল্প কভারড পেরোল পিরিয়ডের জন্য প্রযোজ্য - অন্যান্য সমস্ত খরচের জন্য ব্যবহৃত PPP তহবিলগুলি অবশ্যই স্ট্যান্ডার্ড কভারড পিরিয়ডের সাথে ট্র্যাক করা উচিত), তবে কিছু ব্যবসার জন্য, অতিরিক্ত নমনীয়তা এবং অতিরিক্ত বেতনের খরচ যা ক্ষমা গণনাতে অন্তর্ভুক্ত করা যেতে পারে। জটিলতা যোগ করা হয়েছে।

যাইহোক, অন্যান্য ব্যবসার জন্য যেগুলি 'নিয়মিত' কভারড পিরিয়ডের মধ্যে সর্বোচ্চ সম্ভাব্য ক্ষমা পাওয়ার জন্য বেতনের খরচের জন্য যথেষ্ট খরচ করে, বিকল্প কভারড পেরোল পিরিয়ডের নির্বাচন অপ্রয়োজনীয় জটিলতা যোগ করে এবং ব্যবহার করা উচিত নয়৷

Nerd Note:

বিকল্প কভারড পেরোল পিরিয়ড এমন পরিস্থিতিতে ব্যবহার করার সম্ভাবনা নেই যেখানে 24-সপ্তাহের কভারড পিরিয়ড ব্যবহার করা হয়। এই ধরনের কভারড পিরিয়ডগুলি, তাদের নিজস্বভাবে, বেশিরভাগ ব্যবসাগুলিকে সর্বাধিক ক্ষমা অর্জনের জন্য বেতনের খরচে যথেষ্ট পরিমাণে বেশি ব্যয় করার অনুমতি দেওয়া উচিত (তবে ক্ষমা হ্রাস এড়াতে নিয়োগকর্তাকে দীর্ঘ সময়ের জন্য হেডকাউন্ট এবং বেতন বজায় রাখতে হবে, নীচে আরও আলোচনা করা হয়েছে। )।

পেচেক সুরক্ষা কর্মসূচির (পিপিপি) জন্য যোগ্য খরচ লোন ক্ষমা করা হয় বা দেওয়া হয়

CARES আইনের ধারা 1106(b) একটি ব্যবসার খরচ বর্ণনা করে যা PPP ঋণের পরিমাণ নির্ধারণ করার সময় বিবেচনা করা হয় যা ক্ষমা করা যেতে পারে। বিশেষ করে, ধারা 1106(b) বলে:

উল্লেখযোগ্যভাবে, SBA এবং ট্রেজারি দ্বারা প্রদত্ত পরবর্তী নির্দেশিকাতে, PPP ঋণের অর্থ কীভাবে সাধারণভাবে ব্যবহার করা যেতে পারে তার জন্য গৃহীত বিধানের অনুরূপ ক্ষমা গণনার জন্য একটি বিধান গৃহীত হয়েছিল। এইভাবে, মাফ করা পিপিপি ঋণের পরিমাণের অন্তত 60% অবশ্যই বেতন খরচে ব্যয় করতে হবে , ভাড়া, বন্ধকী সুদ, বা ইউটিলিটিগুলিতে ব্যয় করা মাফ পরিমাণ 40% সীমাবদ্ধ করে৷

অবশ্যই, যে ব্যবসাগুলি কেবলমাত্র তাদের আয়ের 100% পে-রোল খরচে ব্যবহার করে, এটি একটি মূল বিষয়, কিন্তু ঋণগ্রহীতাদের জন্য যারা কভারড পিরিয়ডের সময় শুধুমাত্র পে-রোল খরচের জন্য তাদের আয় সম্পূর্ণরূপে ব্যবহার করতে পারে না – যা হওয়ার সম্ভাবনা বেশি যখন একটি 8-সপ্তাহের কভারড পিরিয়ড ব্যবহার করা হয়, কারণ ঋণের পরিমাণ 2.5 মাসের, বা মোটামুটি 10 সপ্তাহের, পে-রোল খরচের উপর ভিত্তি করে ছিল – PPP লোনের আয়ের ন্যূনতম প্রয়োজনীয়তা কত অবশ্যই বেতনের খরচে ব্যয় করা গুরুত্বপূর্ণ হয়ে ওঠে।

Nerd Note:

উপরের উদাহরণে, $80,000 নন-পে-রোল খরচও $80,000 ÷ $200,000 =ইস্যু করা মোট PPP ঋণের 40% প্রতিনিধিত্ব করে। এবং যেমন আগে উল্লেখ করা হয়েছে, 40% হল PPP ঋণের সর্বোচ্চ পরিমাণ যা নন-পে-রোল খরচের জন্য ব্যয় করা যেতে পারে (ক্ষমা করা হোক বা না হোক)। তদনুসারে, অবশিষ্ট $200,000 – $80,000 (পে-রোল ইতিমধ্যেই ব্যয় করা হয়েছে) - $80,000 (অ-পে-রোল) =$40,000 পিপিপি তহবিল অবশ্যই অতিরিক্ত বেতন খরচের জন্য ব্যয় করতে হবে (কারণ এর ফলে $80,000 + $40,020 =$40,020 হবে মোট পিপিপি তহবিলের 60% প্রয়োজন যা অবশ্যই বেতনের জন্য ব্যয় করতে হবে) .

একটি পিপিপি লোনের কভারড সময়ের মধ্যে যোগ্য খরচের জন্য মঞ্জুরিকৃত অর্থপ্রদান এবং ব্যয়কৃত খরচ ব্যবসাগুলিকে তাদের ব্যবহার করা অ্যাকাউন্টিং সিস্টেমগুলির চারপাশে নমনীয়তা দেয়

পিপিপি ঋণ কতটা মাফ করা হবে তা নির্ধারণ করার সময় কংগ্রেস যে কিছুটা অস্বাভাবিক ভাষা ব্যবহার করেছে তা লক্ষ করাও গুরুত্বপূর্ণ; “নিম্নলিখিত খরচের যোগফল এবং পেমেন্ট করা হয়েছে।" উল্লেখযোগ্যভাবে, অ্যাকাউন্টিংয়ের কোনও "ব্যয় বা অর্থপ্রদান" পদ্ধতি নেই; সাধারণত, খরচ গণনা করা হয় অ্যাকাউন্টিংয়ের নগদ-ভিত্তি পদ্ধতি ব্যবহার করে, যা দেখায় কখন ডলার প্রকৃতপক্ষে ব্যয় করা হয়, অথবা অ্যাকাউন্টিংয়ের উপার্জিত-ভিত্তি পদ্ধতি, যা দেখায় কখন যে কার্যটি ব্যয় তৈরি করেছে তা বাস্তবে ঘটেছে। সুতরাং, প্রাথমিকভাবে, নিয়মটি কী হতে চলেছে তা স্পষ্ট ছিল না! ব্যবসার মালিকরা কি উভয়ের মধ্যে বেছে নিতে সক্ষম হবেন?

শেষ পর্যন্ত, SBA এবং ট্রেজারি মূলত উভয়কেই অনুমতি দেওয়ার সুপার-ব্যবসা-মালিক-বান্ধব নির্মাণ গ্রহণ করেছে অ্যাকাউন্টিং পদ্ধতি ব্যবহার করা হবে... একই সাথে! ভিন্নভাবে বলা হয়েছে, যোগ্য খরচের জন্য PPP তহবিল ব্যবহার করা হয় যতক্ষণ না তারা হয় প্রকৃতপক্ষে আচ্ছাদিত সময়ের বা সময় অর্থ প্রদান করা হয় কভারড পিরিয়ডের সময় খরচ হয়!

একটি ছোট কিন্তু সমালোচনামূলক সমস্যা রয়েছে যা ব্যবসার মালিকদের এই (অবিশ্বাস্যভাবে অনুকূল) খরচের চিকিত্সা ব্যবহার করার জন্য সচেতন হওয়া দরকার। ব্যয় খরচের জন্য কভারড পিরিয়ডের সময় ক্ষমা ফর্মুলার দিকে গণনা করার জন্য, তাদের অবশ্যই পরবর্তী নির্ধারিত বেতন তারিখ/বিলিং তারিখে বা তার আগে পরিশোধ করতে হবে। যদি কভারড পিরিয়ড চলাকালীন কোনো খরচ পরিশোধ করা না হয়, বা খরচ করা হয় কিন্তু তারপরের প্রথম নিয়মিত বিলিং তারিখের মধ্যে পরিশোধ না করা হয়, তাহলে তা না প্রদত্ত বা হিসাবে যোগ্য হন খরচ হয়েছে।

পে চেক দ্বারা সংজ্ঞায়িত যোগ্য বেতনের খরচ সুরক্ষা প্রোগ্রাম (পিপিপি) প্রতারণামূলকভাবে জটিল, বিশেষ করে ব্যবসার মালিকদের জন্য

পেচেক সুরক্ষা প্রোগ্রামটি প্রাথমিকভাবে কর্মীদের নিযুক্ত রাখতে সাহায্য করার একটি উপায় হিসাবে ডিজাইন করা হয়েছিল (বা, যেমন বলা যেতে পারে, কর্মীদের বেতন চেক রক্ষা করার জন্য!)। তদনুসারে, কংগ্রেস কর্তৃক বরাদ্দকৃত পিপিপি তহবিলের একটি উল্লেখযোগ্য অংশ সরাসরি এতে চলে গেছে তা নিশ্চিত করার জন্য একটি উল্লেখযোগ্য সংখ্যক নিয়ম রয়েছে (যেমন ন্যূনতম 60% ব্যয়ের প্রয়োজনীয়তা এবং ন্যূনতম ক্ষমা থ্রেশহোল্ড যা বেতন-ভাতার ব্যয়ের ক্ষেত্রে প্রযোজ্য) em> শ্রমিকরা "পে-রোল।"

কিন্তু যদিও "পে-রোল" শব্দটি "মজুরি" বা "বেতন" এর ধারণাকে উদ্বুদ্ধ করতে পারে, পিপিপি ঋণের উদ্দেশ্যে "পে-রোল খরচ" শব্দটি নিশ্চিতভাবে বিস্তৃত। উদাহরণস্বরূপ, স্ব-কর্মসংস্থান থেকে নেট উপার্জন অন্তর্ভুক্ত করার পাশাপাশি (যারা নিজেদের অর্থ প্রদান করছেন তাদের জন্য মজুরি, কমিশন, বেতন এবং অন্যান্য নগদ ক্ষতিপূরণ সহ ব্যবসার মালিক হিসাবে!

- অবকাশ, পিতামাতার, পরিবার, চিকিৎসা এবং অসুস্থ ছুটির অর্থ প্রদান;

- গ্রুপ হেলথ কভারেজ (বীমা প্রিমিয়াম সহ);

- অবসরের সুবিধা; এবং

- রাষ্ট্রীয় এবং স্থানীয় কর।

However, while these expenses can generally be included in the amount of a PPP loan eligible for forgiveness, and self-employed individuals can even include some of their own earnings from the business as payroll (even if not actually received as a W-2 salary, in the case of partnerships or sole proprietorships), the SBA and Treasury rules limit the ability to include some of these other ‘employee benefits’ payroll-related expenditures if they are made on behalf of business owners themselves (who work at/for the company).

More specifically, the following expenses are not considered Payroll Costs:

- Group Health Coverages, to the extent that costs are for:

- S corporation owner-employees with 2% or more ownership, or their family members;

- Schedule C/F businesses; অথবা

- General partners.

- Retirement Benefits, to the extent that costs are for:

- An owner-employee of a C corporation or an S corporation (excluded only when costs exceed 2.5 ÷ 12 =20.8% of the 2019 contribution made by the employer);

- Schedule C/F businesses;

- General partners.

- State and Local Taxes, to the extent that they are attributable to:

- Schedule C/F businesses; অথবা

- General partners.

Reductions In Loan Forgiveness For Not Maintaining Headcount Or Sufficient Compensation

As noted earlier, the primary purpose of the Paycheck Protection Program was to safeguard the employment status of small business workers. Accordingly, some businesses that received PPP loans, but that failed to adequately protect worker’s compensation, may be ‘punished’ via a reduction in the amount of their PPP loan that is eligible to be forgiven.

Or at least some of them are…

As while the Paycheck Protection Program did originally include requirements for businesses to maintain certain employee headcount requirements to be eligible for forgiveness on their PPP loans, on October 8, 2020, the SBA and Treasury announced that borrowers who received loans of $50,000 or less would not be subject to such reductions in forgiveness. Which, notably, ‘covers’ more than two-thirds of PPP borrowers (but only about 10% of loan dollars). However, borrowers who took larger loans must still deal with a variety of rules that can result in a reduction of the forgivable amount of their loan.

More specifically, reductions in the forgiveness of PPP loan proceeds spent on eligible expenses during the Covered Period are generally applied for both reductions in the number of Full-Time Equivalent (FTE) employees (the number of cumulative 40-hour workweeks a business’ employees perform) during the Covered Period (as compared to a reference period) and reductions in (non-highly-compensated) workers’ compensation in excess of 25% (to prevent businesses from claiming they maintained headcount but then drastically cutting compensation for all the employees they kept on payroll). In other words, businesses had to maintain at least the same number of full-time equivalent employees at the start and end of the Covered Period, and those (non-highly-compensated) employees had to maintain at least 75% of their compensation (i.e., a not-more-than-25% reduction in compensation) to remain fully eligible for PPP forgiveness.

There are, however, a variety of exceptions to the required thresholds of which business owners should be made aware.

Determining How Reductions To Full-Time Equivalent (FTE) Employee Headcount Will Reduce Paycheck Protection Program (PPP) Loan Forgiveness

Some businesses that received PPP loans were able to maintain their employee headcounts and hours throughout their Covered Periods. In such instances, the reward that those businesses receive is the ability to completely ignore this part of the forgiveness process!

Of course, not all businesses – even with a boost from the Paycheck Protection Program – were able to maintain employee headcount. The penalty for not doing so is a reduction in the amount of the business’ PPP loan that would otherwise be forgiven (with some exceptions, discussed later).

More specifically, a business must compare its average weekly Full-Time Equivalent (FTE) Employees during the Covered Period (or, if elected, the Alternative Payroll Covered Period) to its FTEs during either the period from January 1, 2020 – February 29, 2020, or during the period from February 15, 2019 – June 30, 2019. Notably, businesses can pick the more favorable of these periods (the period in which there were fewer FTEs) for the comparison.

In general, to compare the number of average weekly FTEs during the Covered Period and the comparison period, it is necessary to determine the average weekly FTEs during both periods. A standard FTE is equivalent to one 40-hour workweek, regardless of the number of individuals it takes to get to the 40-hour mark. Thus, a single worker who works 40 hours in a single week is equivalent to one FTE for that week. Similarly, if two workers each work 20 hours in a week, they would also constitute, together, a single FTE, as would 8 workers each working 5 hours per week, and so on.

One caveat to this rule, however, is that a single worker cannot comprise more than 1 FTE per week, even if that individual works for more than 40 hours during the week. Thus, while two workers who each work 30 hours per week will constitute (30 x 2) ÷ 40 =1.5 FTEs, a single individual working 60 hours in a week will be equal to just 1 FTE!

Once the numbers of average weekly FTEs during the Covered Period and the comparison period are known, the two amounts must be compared. And, in general, any decrease in the number of average weekly FTEs from the comparison period to the Covered Period will result in a reduction of the forgivable amount of the PPP loan.

For borrowers that do fail to maintain their FTE headcount, the adjustment to their PPP forgiveness is relatively straightforward:the otherwise forgivable amount of the PPP loan will be reduced by the same percentage as the percentage drop in FTEs from the comparison period to the Covered Period. So, for instance, a 20% drop in average weekly FTEs from the comparison period to the Covered Period will typically result in a 20% decrease in the amount of the PPP loan a business received that would otherwise be forgiven.

Safe Harbor FTE Calculation

Incredibly enough, there is yet another election that business owners can choose to make when calculating whether they maintained employee headcount and/or the amount by which their headcount (and thus their forgivable PPP loan) was/is reduced.

Instead of using actual hours worked to calculate FTEs, the business can opt to use a safe harbor method, where all employees who work 40 hours or more during a week are counted as 1 FTE, while all employees who work less than 40 hours during a week are counted as one-half of an FTE.

Perhaps not surprisingly, this is an all-or-nothing decision. A business can’t, for instance, use the safe harbor in some weeks, but not others. Or for some employees, but not others. It’s either used for all the employees for every week of the Covered Period or for none of the employees in any week of the Covered Period.

Using the safe harbor method to calculate FTEs will usually alter the number of FTEs for comparison purposes.

It’s important to note, though, that while using the safe harbor method of calculating FTEs would have resulted in a negative outcome in the example above, its use can actually result in either a positive or a negative effect on forgiveness, depending on the specific set of facts and circumstances.

Exceptions To Reductions In Loan Forgiveness Due To A Drop In FTEs

Although Congress was intent on making sure that PPP loan proceeds were used to keep workers employed through at least the end of the Covered Period, it recognized that there would be some situations where doing so would not be possible, for reasons largely (if not entirely) outside of an employer’s control. In particular, some business owners with lower-wage employees raised concerns that the enhanced unemployment benefits made available as a part of the CARES Act were actually resulting in employees not wanting to return to work until the increased unemployment benefits ended (potentially rendering the employer unable to meet the ‘maintain headcount’ requirement for its own PPP forgiveness).

Accordingly, Congress, the SBA, and Treasury, collectively crafted a series of exceptions to the general rule for reductions in forgiveness. Thus, a business will not have its forgiveness amount decreased for any of the following situations occurring during the Covered Period or Alternative Covered Period:

- The borrower made a good-faith, written offer to rehire an individual that was rejected by the employee;

- The employee was fired for cause;

- The employee voluntarily resigned;

- The employee voluntarily requested and received a reduction in their hours;

- The borrower made a good-faith effort to restore any reduction in hours at the same pay, but was rejected; অথবা

- The borrower tried but was unable to hire similarly qualified employees for unfilled positions by December 31, 2020.

A careful reading of the above exceptions reveals that they are not blanket exemptions for an employer that covers every employee. Rather, they are acceptable ‘excuses’ to ignore a drop in FTE count specific to an individual employee.

By contrast, there are two additional exceptions to a drop in FTEs that can be used broadly, across a business, for all employees. They are when either:

- The borrower is able to document an inability to return to the same level of business activity as such business was operating at before February 15, 2020, due to compliance with requirements established or guidance issued by the Secretary of Health and Human Services, the Director of the Centers for Disease Control and Prevention, or the Occupational Safety and Health Administration during the period beginning on March 1, 2020, and ending December 31, 2020, related to the maintenance of standards for sanitation, social distancing, or any other worker or customer safety requirement related to COVID–19; অথবা

- The borrower reduced its number of FTEs between February 15, 2020, and April 26, 2020, but restored its FTE count by the earlier of December 31, 2020, or when its application for forgiveness is submitted.

For certain businesses, these two exceptions to the ‘normal’ FTE reduction rules can be huge. They are effectively ‘get-out-of-jail-free cards’ that will eliminate any and all FTE reductions that would otherwise apply (though PPP funds will still need to be spent on eligible expenses during the Covered Period to be eligible for forgiveness).

For businesses that are unable to return to the same level of business activity as before February 15, 2020, due to compliance requirements, it’s as simple as documenting the public health requirement and the corresponding drop in business activity (read “gross revenue”).

Meanwhile, for businesses that reduced employee headcount or hours at some point between February 15, 2020, and April 26, 2020, it just needs to reverse those decisions by the end of the year. Thus, now may be a critical time for such businesses to consider bringing back employees, as the difference between rehiring staff on December 15, 2020, for example, and January 15, 2021, could be the difference in thousands (or even tens or hundreds of thousands) of additional forgiveness!

Reductions In Loan Forgiveness For Large (Greater-Than-25%) Cuts In Compensation To Non-Highly Compensated Employees

If not for an additional restriction, shrewd business owners may have looked to avoid drops in headcount by simply cutting employees’ compensation but keeping them employed. However, while certain cuts in compensation are allowed, the CARES Act does limit such actions.

More specifically, to the extent that an employee with annualized salary/wages of less than $100,000 during 2019 has their compensation slashed by more than 25%, the excess (beyond 25%) will result in a dollar-for-dollar drop in the amount of the business’ PPP loan that is forgivable (unlike the reduction due to employee headcount, which is calculated on a percentage basis). This dollar-for-dollar reduction in the PPP forgivable amount due to a reduction in employee compensation is made by comparing the drop in wages/salary during the Covered Period to the average salary/wages paid to the employee from January 1, 2020 – March 31, 2020.

However, cuts in compensation of less than 25% to the same employees have no impact on forgiveness. Similarly, cuts to compensation of those earning $100,000 or more in 2019 have no impact.

Two final points are worth mentioning here. First, similar to the ‘exception’ that allows an employer to rehire a terminated individual by December 31, 2020, to avoid a reduction in forgiveness due to a drop in headcount, so too can an employer avoid a reduction in loan forgiveness for cutting a non-highly-compensated employee’s compensation in excess of 25% if the salary is restored by the same December 31, 2020 deadline.

However, per the instructions for forgiveness published by the SBA and Treasury, this exception only appears to be available if the decision to slash wages/salary was made between February 15, 2020, and April 26, 2020. (Whereas subsequent reductions in compensation or headcount that were implemented after April 26

th

can’t be ignored, even if the employees are subsequently re-hired or restored to their prior compensation level.)

Second, a business that both reduced its FTEs and cut non-highly compensated employees’ wages by more than 25% will have two reductions in the amount of its PPP loan that would otherwise be forgivable.

There is, however, an “order of operations” that must be followed. More specifically, the dollar-for-dollar reduction for salary cuts (to non-highly-compensated employees) is applied first, followed by applying the percentage reduction in forgiveness due to a drop in FTEs to the already reduced amount.

Strategies To Help Maximize Paycheck Protection Program (PPP) Loan Forgiveness

As is plainly evident, the rules for determining the amount of a business’ PPP loan that can be forgiven by the SBA are complicated (one might even say “obnoxiously” complicated!). That complexity will inevitably lead to some business owners failing to get the maximum possible amount of their PPP loan forgiven or lead to other planning complications.

Advisors can, and should, help clients avoid this fate by taking steps that include the following:

- Choose the Covered Period Wisely – As noted earlier, PPP borrowers who received their loans prior to June 5, 2020, have the flexibility of choosing either an 8-week or a 24-week Covered Period. This covers the majority of borrowers and provides for ample planning opportunities.

Where the borrower maintains their employee headcount and wages through the ‘regular’ 8-week Covered Period (or qualifies for an exception to forgiveness reductions) and expends enough on payroll (and, if necessary, on other expenses) to have the full PPP loan forgiven (which is pretty likely, if full employment was maintained), the 8-week Covered Period is the logical option.

If this isn’t enough to get full forgiveness, but the business is otherwise relatively close to the required expenditures to obtain full PPP forgiveness, the next step is to see if the Alternative Payroll Covered Period is enough to do the trick.

If the Alternative Covered Period allows the business to spend enough on eligible expenses to get maximum forgiveness, then using it is a ‘simple’ solution.

If it doesn’t, it’s necessary to explore the 24-week Covered Period option instead. If the borrower maintains headcount and wages through the ‘extended’ 24-week Covered Period (or qualifies for an exception to forgiveness reductions), then this becomes the logical option.

However, if FTEs are not maintained and/or there are significant (<25%) cuts to the wages of employees with annualized compensation of less than $100,000, further analysis is warranted.

At the heart of the matter lie two questions…

- Does the added time of a 24-week Covered Period allow the business to spend enough on qualifying expenses, such that including these expenses would more than offset any additional reductions in forgiveness due to a drop in FTEs or cuts to non-highly compensated workers’ wages that might have also occurred during the 24-week period?; এবং

- Would the added reductions to forgiveness due to declines in FTEs or cuts to non-highly compensated workers’ wages more than offset any gains from the inclusion of additional expenses?

If the answer to question 1 is “yes” and the answer to question 2 is “no”, then extending to the 24-week Covered Period likely makes the most sense. Otherwise, keeping the ‘original’ 8-week Covered Period will probably be more beneficial for the borrower.

Unfortunately, there is no easy way to figure this out. Someone must ‘run the numbers’ using each method and see what the best result is!

- Make Smart Decisions If Reductions In FTEs And/Or Employee Compensation Are Required – There are a lot of ways to try and mitigate the impact of reductions in headcount or payroll for business owners who truly understand the PPP forgiveness rules. Options for business owners who received PPP loans of greater than $50,000 (and thus, subject to the reduction rules) include the following:

- Keep wage cuts to no more than 25% for those employees with annual wages of less than $100,000;

- Where more significant cuts to wages are required, cut the wages of employees with annual wages in excess of $100,000;

- If additional hours are required above 40 hours per week for a particular role, try to hire additional employees (even on a part-time basis) to do the work because their hours will count towards the FTE requirement (while having the original employee work in excess of 40 hours per week won’t add to the FTE count);

- Run FTE calculations using both the ‘regular’ calculation and the safe harbor method; এবং

- When the safe harbor FTE calculation is used, minimize the number of employees working between 20 and 39 hours per week (no additional credit is received).

- Prepare Clients Receiving Substantial Forgiveness For A Bigger Tax Bill! – In the event that a business owner is able to successfully navigate the PPP forgiveness rules to have all or a large portion of their PPP loan forgiven, it’s a substantial win for the business owner. But it’s not a total win… at least not yet.

More specifically, while Section 1106(i) of the CARES Act stipulates that “any amount which (but for this subsection) would be includible in gross income of the eligible recipient by reason of forgiveness described in subsection (b) shall be excluded from gross income,” the IRS has effectively negated this position by disallowing any expenses paid with forgiven funds from being deductible by a business on its return.

Without such deductions, the profit of some businesses may be ‘artificially’ inflated, leading to higher-than-normal tax bills for business owners.

The last thing anyone wants is an unexpectedly large tax bill. But given the pandemic and the struggles many business owners are already dealing with, that may never be truer than today. Advisors, therefore, must help such clients plan ahead and avoid surprises.

The CARES Act provided a massive stimulus to the American economy in response to the worst pandemic in more than 100 years that gripped the nation. Included in the stimulus was the creation of the much-hyped Paycheck Protection Program, which ultimately provided more than half a trillion dollars in loans to business owners in an effort to help them maintain their employee headcount and payroll.

But while the PPP loans, themselves, have been valuable for business owners, the real cherry on top has been the ability to have some, if not all, of the loan forgiven by the SBA. To benefit from this, though, business owners need to navigate a complex web of rules, from understanding various Covered Periods to knowing what expenses count towards forgiveness – a particularly cumbersome issue for business owners themselves – to dealing with reductions that can apply when employee headcount and/or wages are not maintained throughout the Covered Period.

The good news for advisors is that this complexity provides ample opportunity to educate clients and to provide invaluable guidance in a time of great need. Doing so not only helps business owners to maximize the amount of PPP forgiveness they receive, but can also create the kind of goodwill that can lead to clients for life!